t’s already been a banner year for VCs and we still have three months to go. That’s the takeaway from the Venture Monitor report, published by PitchBook and NVCA this morning. Let’s break out the “space tech” investment data.

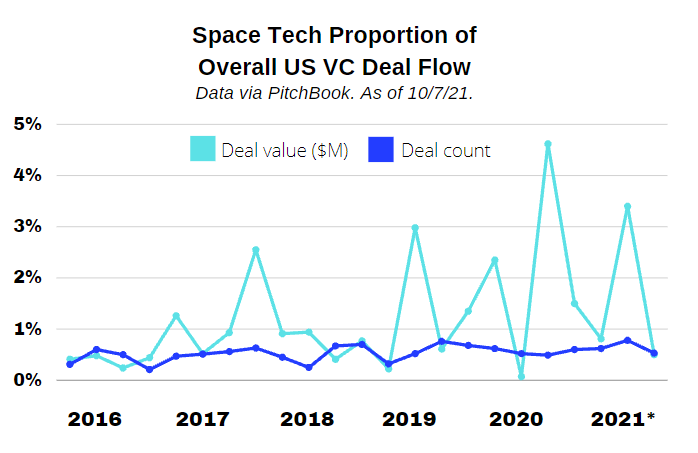

Since 2016, space tech has accounted for ~1.2% of all VC funding. That proportion jumps around in quite erratically, as you can see above, due to episodic mega-deals.

We’re unsure where to draw the line at what is and isn’t a mega-deal. We’ll leave that to you. But here are the top deals so far this year, ordered by size:

- SpaceX, ~$1.2B (April)

- Relativity Space, $650M (June)

- Astranis, $281M (April)

- ICON Technology, $207M (August)

- ABL Space Systems, $170M (March)

- Axiom Space, $130M (February)

- Climavision, $100M (June)

- Tomorrow.io, $77M (March)

- Firefly Aerospace, $75M (April)

- Orbital Insight, $73M (May)

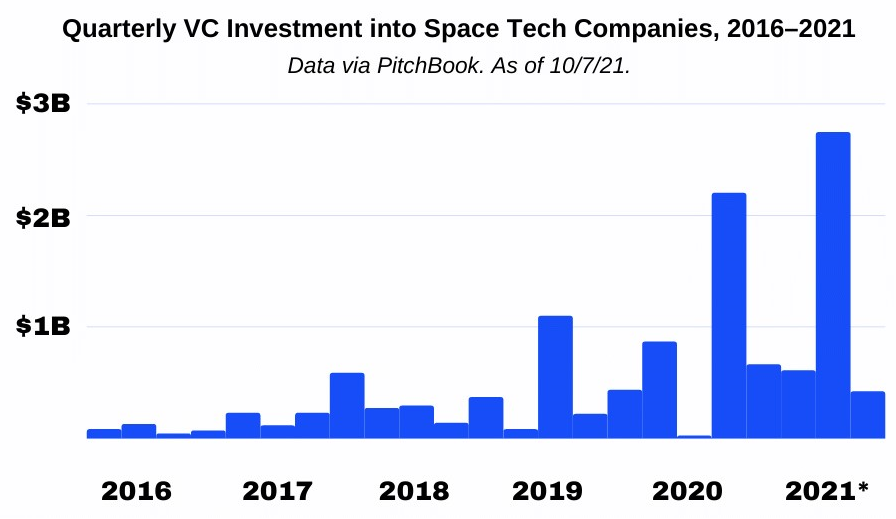

Total quarterly investment is also heavily impacted by mega-deals. In this graph, you can also see the pandemic’s effect on space investing very clearly:

Sierra Space Closes $550M Series C

LuminArx Capital led the round, which valued the company at $8B.

Vast Secures $500M, Including $300M Series A

Vast has closed a $300M Series A to continue production of its Haven commercial space station, the company announced this morning.

ISPTech Raises €5.5M to Scale Green Propulsion Tech

Green energy is all the rage in Europe, and the trend is beginning to reach beyond the stratosphere.

Canada’s NordSpace Opens VC Arm for Sovereign Space Investments

The company today launched NordSpace Ventures, which will make investments in “Canadian space, defense, and dual-use technologies”—starting with Wyvern, an EO company based in Edmonton, AB.

This morning, Spaced Ventures (SV) announced a $1.2 million seed round led by WorldQuant Ventures. Founded one year ago, the startup recently opened its space crowdfunding platform to the public in beta mode.

“There’s been this old narrative that crowdfunding is for the leftovers, the companies that aren’t good enough,” SV CEO Aaron Burnett told Payload. “We think that narrative’s being torn down.” SV’s business is made possible largely thanks to Reg. CF, a relatively recent SEC rule allowing startups to raise $5 million via crowdfunding offerings every year.

Freshman class…SV currently has three startups listed on its investment portal:

Keep reading