The space industry has grown rapidly in recent years, and a new report from Novaspace suggests that things are just getting started.

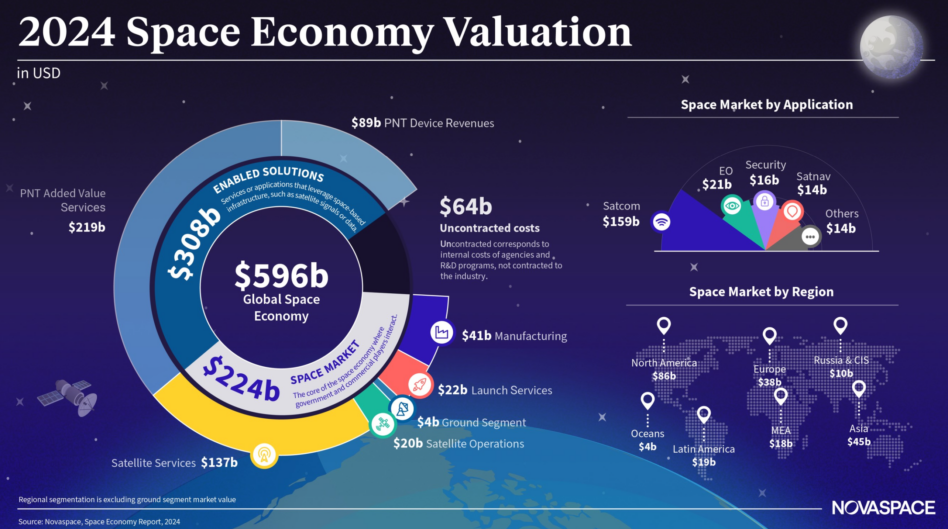

The report, released yesterday, predicted that the global space economy will reach $944B by 2033. The growth will be primarily driven by the increased adoption of downstream technologies such as AI and cloud computing, which make space data more accessible to businesses. In 2024, the global space economy was valued at $596B—meaning if their prediction is true, the industry will grow by 1.5 times in fewer than 10 years.

Snapshot: Novaspace’s gauge of the space economy in 2024 revealed that downstream solutions—the services and applications which leverage space-based infrastructure and data—already account for over half of the current valuation. The upstream sector, by comparison, includes launch, satellite manufacturing, and ground stations.

As more hardware heads to orbit to provide these capabilities—from advanced EO sats to satcom megaconstellations—terrestrial companies get more and more data to analyze and sell.

This reality is most stark in Asia, where satellite services make up nearly two-thirds of the space industry. In a region where sovereign launch and manufacturing is either relatively new or nonexistent, the satellite services market has carved out a name for itself by leveraging the space data generated on orbit.

The projected growth, however, isn’t guaranteed. Inflation, supply chain disruptions, and the success or failure of new entrants in the launch sector remain barriers for the space economy to reach its full potential.

Follow the money: While the commercial sector is driving value in the overall space market’s valuation, government spending in that sector remains a pivotal source for future growth. Luckily, governments around the world are stepping up their military space budgets, which currently exceed $64B worldwide—generating contract opportunities for business.

For now, the US dominates the space market, comprising the largest market share for both upstream capabilities (launch, satellite manufacturing, and ground segment operations) and downstream capabilities (satcom, EO and PNT) globally.

However, the future may see a more evenly distributed global market, as government spending on space in the EU and Asia grows at a faster rate than in the US—which is currently mulling the largest NASA funding cut in the country’s history.

Who’s Working With China on Space?

“Africans don’t choose sides, at least for now…so these countries are typically not locked into one provider,” said Mustapha Iderawumi, a senior analyst at Space in Africa—a Lagos, Nigeria-based market research firm.

ICEYE Smashes Its Own Revenue Projections

ICEYE’s results reveal a massively successful year for a business in the right place at the right time.

Anduril To Acquire ExoAnalytic

Anduril Industries announced this morning that it will acquire ExoAnalytic Solutions—a move that will double the neo prime’s space headcount.

Astrobotic Wins Lunar Wheel Contract For Italian Habitat

The Pittsburgh, PA-based space firm won a contract of undisclosed value from Thales Alenia Space to contribute the wheels for Italy’s Multi-Purpose Habitation.

It’s time to play the game again! On Friday, the White House released top-line budget numbers that covered key space spenders at DoD and NASA. While there’s no guarantee this is what the final budget looks like, here’s our guide to the people, companies and concepts that stand to gain, and those that are in trouble.

The high-level budget proposal reflects who has leverage in Trump world.

SpaceX CEO Elon Musk: Entirely by coincidence, Musk’s perch in the White House led to a lot of advantageous spending for his company. Massive cuts at NASA aren’t touching the programs SpaceX is committed to, while Musk’s Mars agenda will get a $1B increase. The company seems poised to benefit from proposed cuts to legacy Moon-landing tech and is reportedly the frontrunner in the DoD’s push for new space-based missile defenses.

Keep reading