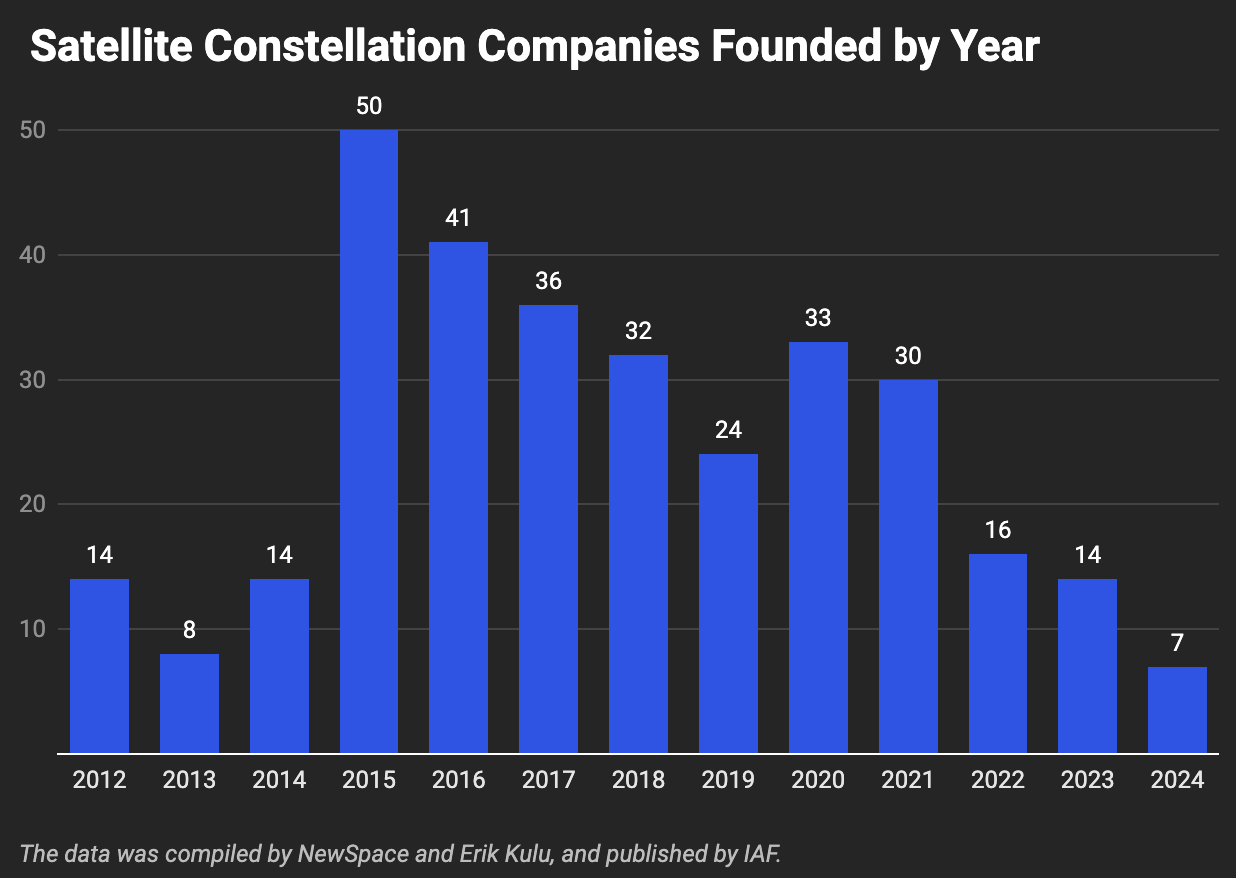

The number of new satellite constellation businesses has sharply declined over the past decade as the space market matures and new startups struggle to find angles to differentiate.

In 2024, only seven new constellation businesses (i.e., satcom, EO, and in-orbit inspection satellites) were founded globally, according to NewSpace.

In 2015, that number was 50.

Why the 2015 boom? The LEO economy burst onto the scene in a big way in 2015. That year SpaceX secured $1B of funding; OneWeb raised $500M; and Planet Labs closed a $118M round.

- Compare that to recent raises: The largest US funding round over the past two years was Axiom’s $350M raise in 2023.

2015 was also the year SpaceX landed its Falcon 9 booster for the first time.

Excitement over the new LEO economy—and its investor interest—drove a constellation gold rush with dozens of new businesses entering the market. Although there was a brief resurgence during the space SPAC boom of 2020-2021, that trend has been unwinding ever since,

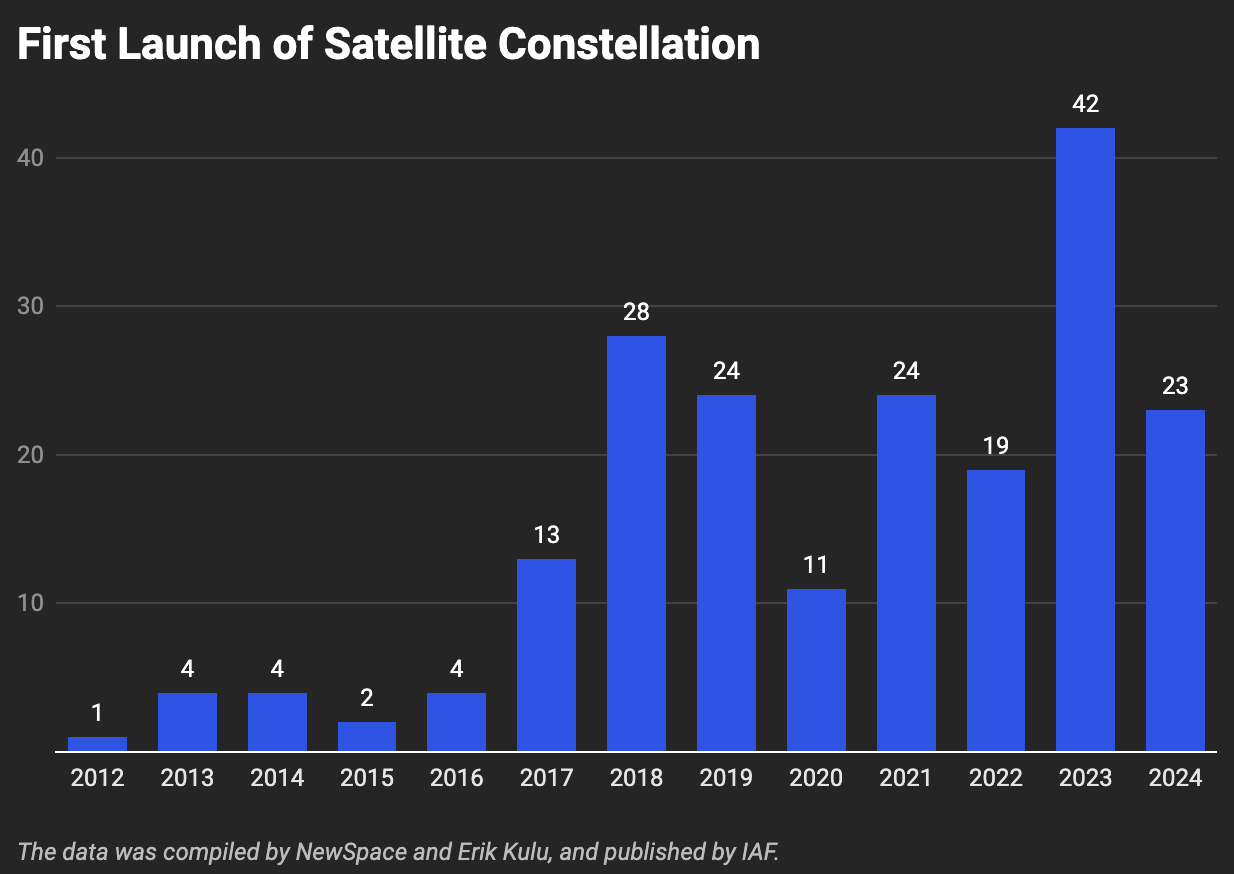

The irony: The irony of the down and to the right graph is that if we superimpose the trendline of the space economy over the past decade, it would show a healthy incline.

One reason for this is the delay (usually 3 to 4 years) between a company’s founding and putting hardware in orbit. You can see the lag clearly in the graph below of the first launch of satellite constellations.

- 2018 was a big year for first-time launches (3 years after 2015)

- Similarly, 2023 was a big year for first-time launches (3 years after 2020).

However, the primary driver for the steep fall off in constellations company foundings is that the market is maturing. Many of the winners (and the losers) have been picked; at least in this era of the space economy.

It happens in every emerging industry.

- When a new market opens, new entrants flood in, thinking their approach is best.

- Startups who are able to execute with the best and least expensive tech rise to the top and begin to take advantage of economies of scale.

- The startups that stumble too often, or cannot find a niche, are wiped out.

Seeing the graveyard of bankrupt competitors and the dominance of entrenched players, new entrepreneurs will then refrain from entering the market—that is, until they can find an angle to differentiate and disrupt.

Where is the need? The issue is that over the past few years, entrepreneurs have struggled to identify that differentiating angle. Investors are hesitant to back a run-of-the-mill EO or satcom startup that will have to compete intensely on pricing with established competitors. The result is a chart of declining new companies founded.

“Many space-related businesses resemble utilities: payloads to space ($/kg), bits to, from, or within space ($/MB), energy from space ($/kW-hr), imagery ($/pixel), and it is very, very hard to build a monopolistic business as a utility,” a VC investor told Payload last year.

The Rivada example: A good example of this dynamic is Rivada’s splashy announcement in 2022 that it was targeting a 600-bird broadband mega constellation, competing directly with Starlink, OneWeb, and soon-to-be Kuiper, Telesat, and IRIS².

Rivada’s plans were met with speculation, and three years later, they still have not been able to convince investors why yet another mega broadband constellation was needed. The project remains in an indefinite holding pattern.

Getting a Constellation off the Ground

The emergence of SpaceX’s transporter missions in 2021 allowed for many of the 400+ constellations that NewSpace tracks to get off the ground with at least a tech demonstrator. But the transition from prototype to full-scale deployment has proven hard to fund and execute.

- This is evident in the strong demand for Falcon 9 Transporter rideshare missions (you can’t book a ride until 2027).

- But relatively weak demand for full-on dedicated Falcon 9 launches (there have been only ~20 dedicated commercial customer LEO launches over the past three years).

NewSpace reports that roughly:

- 5% of constellations have been launched/or replenishing

- 14% are in the process of being launched, but slowly

- 21% have launched prototypes

- 30% are in development phase

- 29% have been canceled or are dormant

On the satcom side, you have Starlink, OneWeb, and Iridium, which have achieved constellation scale. On the EO side, only Planet and Spire have launched over 50 satellites—although companies like BlackSky, Satellogic, ICEYE, HawkEye 360, Capella, Umbra, and Maxar have been able to deploy satellites at their desired scale.

New, New Space

There are a few market catalysts that could encourage both constellation growth and new entrants into the market.

- Satcom: Over the past three years, Starlink has introduced satellites to the broader consumer public, expanding the market past what was previously enterprise-only. Additionally, emerging tech such as direct-to-device and data relay could provide further catalyst for growth and innovation.

- EO: The intersection of AI + EO data, the introduction of the VLEO domain, strong defense adoption, and niching off specific end markets can spark new momentum in the sector.

Then there are the mega reusable rockets.

New paradigm: While Falcon 9 and commercial rockets opened up the LEO economy, introducing fully reusable rockets such as Starship, New Glenn, or even Stoke Space’s Nova could usher in the next iteration of the space economy. The potential for lower cost and mass requirements could upend design constraints that traditionally informed constellation companies and offer a window for new constellation companies to be founded.

Exclusive: Tilebox Launches AI-Focused Update

Tilebox announced an update today aiming to make AI agents more effective geospatial-data analysts.

Recapping Planet’s Q1 With CFO and President Ashley Johnson

“That’s one of the ways that I think we’re differentiated from companies that are going to have much more binary outcomes,” she said. “If you’re selling hardware, you recognize revenue when you’ve delivered that hardware. If it fails, that’s the end of the story.”

Bellatrix Aerospace Tapped to Build Korean VLEO Demo Sat

Bellatrix Aerospace is teaming up with Korean optical payload manufacturer TelePIX on a new VLEO demo satellite, launching NET 2028.

Satellogic Lands $18M+ Defense-Monitoring Contract

The contract marks the company’s first large agreement since it made that strategic shift to persistent-monitoring capabilities.

The sci fi dreams—and economic boom—that would be fulfilled by establishing a long-term lunar presence all hinge on one thing: the ability to locate, extract, and process water ice on the Moon’s surface.

Two missions are set to launch today that are hoping to take one giant leap towards making that possible.

The missions: Intuitive Machines’ second Nova-C lunar lander, named Athena, and NASA’s JPL Lunar Trailblazer satellite will spend about a week in transit to the Moon, the first step on their journey to better understand the presence of water ice on and beneath the lunar surface.

Keep reading