Former Google chief Eric Schmidt took over as CEO of Relativity earlier this month after investing a billionaire’s bounty into the struggling rocket startup.

Once valued at over $4B, Relativity hit a liquidity wall in November as mounting costs stemming from its big-bet pivot from its small launcher Terran 1 vehicle to its heavy-lift reusable Terran R drained company resources.

Billionaire rocket club: Schmidt’s commitment, with a net worth over $30B according to Bloomberg, could exceed $1B, a source told Payload.

With that, Relativity is once again back on the short list of US rocket companies with the funding and tech development to have a fighting chance in the years ahead. Other names on the list include household names like SpaceX, ULA, Rocket Lab, Firefly, Blue Origin, and Stoke. Outside of the established companies, investment in small US launchers has slowed to a crawl, forcing dozens of companies to go dormant, or pivot to defense.

- In 2017, 27 new small launchers (less than 1,500 kg to LEO) were founded, according to data from the NewSpace Index.

- In 2023, only four were founded.

There are still fledgling launchers that garner substantial investor interest abroad, given the need for sovereign capability. Nonetheless, new launcher foundings across the board have been dropping precipitously since 2017 as the market solidifies.

The decline in new launcher foundings follows a similar downward trend of new satellite constellations over the past decade.

Charting the decline:

- A burst of optimism around the potential for a LEO space economy in 2015 drove a spike in investment in the infrastructure layer (launch) and the platform and application layer (satellite constellation services).

- Like constellation businesses, the rocket market has since matured. A handful of companies were able to execute and raise the billions needed to get to maiden launch. But most didn’t. And investors, seeing a solidifying market often backed by billionaire pockets, were no longer willing to throw good money after bad.

It takes a long time (usually at least 5 years) and a staggering amount of capital (hundreds of millions, if not billions of dollars) to stand up a rocket. SpaceX, Rocket Lab, Firefly, and Blue Origin are the only operational rocket startups in the US. Relativity and Stoke are still a year or two out (ULA is a Boeing-Lockheed JV, not a startup).

Of the four operational launch startups, only Firefly was founded after 2015; the other three businesses were founded between 2000 and 2006.

Path to operational: According to the NewSpace Index, of the 214 small launchers founded since 1990, only 16% have turned operational, and just 10% are active today. More names will be added to the active list in the next few years, but most have, or will, putter around in yearslong development and capital-raising tours before moving into the dormant/canceled category.

The low probability doesn’t necessarily scare off VC investors who live and die by the Power Law, where one or two investments generate the majority of a portfolio’s returns, and the rest are OK to be zeroed out.

However, the business headwinds don’t stop at turning a rocket operational.

- Small launch is largely a solved problem. Today, if smallsat and cubseat operators want to get to orbit, they can call up Firefly for an Alpha ride or Rocket Lab for an Electron flight or hitch a ride on a SpaceX transporter mission.

- Also, even if a rocket startup gets to operational status, it’s still likely to face years of additional funding needs, delays, and ka-boom setbacks until it can reach a reliable cadence and positive cash flow. It has also yet to be proven whether a small launch provider can achieve profitability on its own.

Getting the business model right: Rocket Lab, the most prolific small-launch provider, does not have a path to profitability with Electron alone. Management has determined that medium-lift Neutron is the way forward. Likewise, SpaceX launched small-lift Falcon 1 only five times before pivoting to Falcon 9. Even with 100 Falcon 9 launches a year and generating 75% margins on launch due to reusability and Starlink subscription revenue, SpaceX barely breaks even.

The bearish investment climate for new rocket startups has had the effect of thinning the launch market. And if commercial aerospace is any comparison, further culling and consolidation in the US may lie ahead.

Internationally, however, sovereign launch capability is a key national security priority, creating opportunities for new commercial launchers abroad.

International Launchers

Germany-based Isar Aerospace is one day away from the maiden flight of its Spectrum rocket, capable of carrying 1,000 kg to LEO. The company has raised over $400M. Other European launch startups, including Rocket Factory Augsburg (Germany), HyImpulse (Germany), Orbex (UK), Skyrora (UK), HyPrSpace (France), and PLD Space (Spain), have each raised significant funding in a bid to become a Europe’s first successful rocket startup.

ESA released its European Launcher Challenge program this week, which could provide up to €169M ($182M) in funding for each winning company.

Outside of Europe, India, and China have also seen robust funding and new launcher foundings in the past few years. Three of the largest 15 space fundings last year were Chinese launch businesses.

SpaceX Alum Have Raised $9.2B, New Data Shows

As an organization that’s employed thousands of engineers in its 24-year history, SpaceX has acted as both a breeding ground for high-level engineering talent, and as a launch pad for new ideas.

European Space Firms Raised €1.4B of Private Capital in 2025

Private European capital markets are increasingly comfortable backing space-industry upstarts.

Astra Targets Golden Dome With Small Rockets, Says CEO Chris Kemp

“We’re going to do target practice. We’re going to make the clay-pigeon rocket,” Kemp said. “That’s great, because that will drive scale for us…and allow us to bring our cost down for commercial customers, and other government customers.”

SDA Needs Better Planning, GAO Says

In a report released this week, the watchdog agency was unimpressed with the SDA’s planning for the Proliferated Warfighter Space Architecture (PWSA).

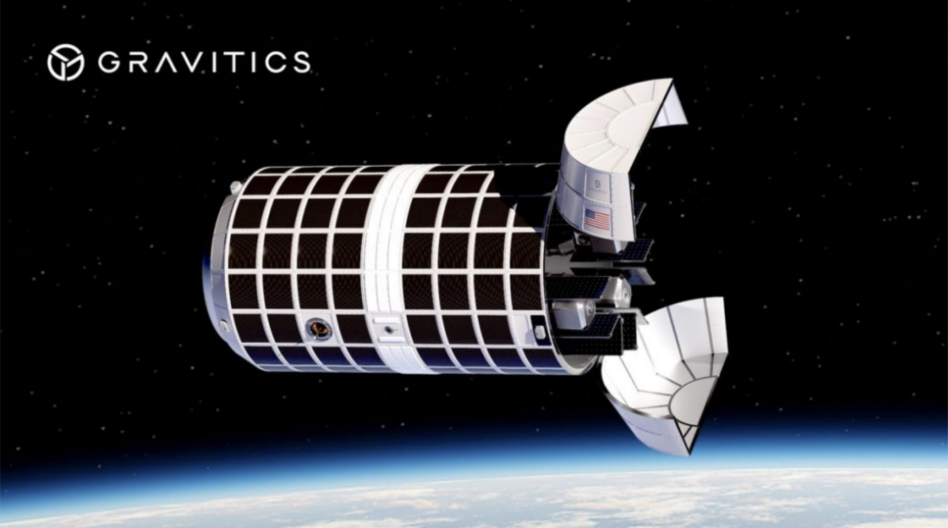

Gravitics, the Seattle-based space infrastructure startup, won a Space Force STRATFI contract worth up to $60M to demonstrate its Orbital Carrier, which is capable of pre-positioning military assets in space for tactically responsive deployment.

Gravitics expects to demonstrate Orbital Carrier’s ability to operate in space and deploy assets on orbit as early as next year.

Whatever it takes: The contract is just one piece of an overarching Space Force effort to boost America’s military posture on orbit in response to the increasing capabilities of Russia and China.

Keep reading