Matthew Desch is the CEO of Iridium (NASDAQ:IRDM), a $5.1B satellite operator based in McLean, VA. Payload recently caught up with Desch across town at Satellite 2022. Over the course of an hour, we chatted about (shocker) satellites, constellation strategy, corporate reinvention, Iridium’s moat, “commodity broadband,” Ukraine, dual-use tech, SPACs, and more.

There are three certainties in life: death, taxes, and satellite operators going bankrupt. And Iridium is no exception to the rule.

- That was then…Iridium filed for Chapter 11 in 1999 after sinking billions into a constellation. At the time, it was one of the 20 largest bankruptcies in US history. A group of investors rescued Iridium, and eventually, the satellite company went on to go public a second time—via SPAC—in 2009.

- And this is now…Iridium’s LEO constellation provides specialty services over the L band. Last year, the company generated $245M in pro forma free cash flow. Iridium works with a partner network of 500ish companies, has operating margins north of 60%, and is steadily growing service revenues and its subscriber base.

NB: This interview was edited for clarity and length. But it’s still quite long. We’ve included shortcuts to two top-of-mind topics, if you’d like to leapfrog past the constellation chatter, space multiples, and corporate strategy…

→ Click here to jump to Ukraine → Click here to jump to SPACsThis week, you announced low-bandwidth video streaming on your Certus platform. As low as 4 Kbps to or from anywhere in the world, if I’m not mistaken. You obviously didn’t need to launch new satellites to enable that. What was the key unlock: hardware, software, or the partners you’re working with?

Our strategy is to bring as much capability to as many highly mobile devices as we can. As I said yesterday, a lot of other mega-constellations, the Ka and Ku-band ones, are going big…with big pipes and big devices.

We’re going small and asking how small we can be to deliver a usable package. Our first products were the fastest in the L band, but didn’t compare in any way to a VSAT [very-small-aperture terminal].

It’s a very efficient way of delivering a product that could be a few thousand dollars instead of many thousands of dollars. Even 700 Kbps isn’t the speed we’re used to at home. While it’s great for L, it’s not perfect for video transmission…and certainly not HD video.

But that’s not what we were built for. Under Certus, we’ve scaled down products to be smaller and less expensive, from ~200 to 100 Kbps. Those aren’t video quality links, but our customers want to put video over it. Both companies we announced partnerships with came to us and said: “Well, you don’t have the fastest pipe. You may not have to suffer in terms of functionality of your customers if you use our special compression algorithms that can take video and do magic with it over very low-bandwidth pipes.” And we did a big DoD demo in the Arctic last year that really blew everybody away.

This thought is just occurring to me now: Traditionally, when we talk about space allowing us to put eyes in more places and see more of the world, it’s satellite imagery. But this capability opens up more visibility—via video streaming to or from wherever—through new and non-traditional means.

Some of the biggest innovations happen when you have constraints. If you have unlimited bandwidth, then people get sloppy. Nobody writes tight code or tight software. But satellite networks have limited capacity. Even the biggest networks are still limited. Look at Starlink. Despite perhaps 10,000 to 15,000 satellites, they won’t be able to serve everyone. It’ll still be a limited resource overall, over any given area.

We’re the same way. Companies that can make products that remove constraints or limitations are going to do very, very well. There will be a lot of interesting applications for all kinds of this video: security and surveillance video, game video, and FaceTiming from unique point-to-point locations, to name a few. You don’t have to lug a giant antenna and have a multi 100-gigabit connection. Now, you can carry around a device that runs on battery power and stream video.

How do constellation operators close the business case in 2022? How would your answer now be different from what you’d say if I asked the same question 25 years ago?

The cost of building a network has gone down by maybe a third. I think a half is probably too much, but it’s somewhere in that range.

And I’m talking apples to apples. 25 years ago, satellites were expensive and built to last 12–18 years. You could typically get 15–20 years. Now, people build cheap satellites that don’t last very long. You have to go through 3–4 launch campaigns to get the same 20 years out of them. You need to relaunch and refresh the constellation much more frequently. The argument is that technology rapidly improves and you can make new satellites better.

Launch prices have come down from the days of Delta and Atlas, let’s say by half. But they haven’t come down in the last 10 years, since the Falcon 9 set a new standard. Everybody is still pricing around that.

So, how do you close the business case? It’s still a huge challenge. You have to build the network from scratch, get it up there, and probably go through multiple iterations even before you get enough customers. You’ve got to hope there aren’t too many other people trying to do the same thing.

Because pricing becomes a race to the bottom?

This is a challenge for the megaconstellations and things like the narrowband IoT constellations. Prices are low and volumes must be high. You have to fill your capacity do so on a sustaining basis, while also hoping prices don’t drop because of too much competition. There’s nothing magical about it: You price to whatever you can get and win the business you need. Hope springs eternal. But I’d say the biggest technology everybody needs to employ to achieve a business case closure is patience.

*chuckles* So, patience is a technology.

It took 25 years and two generations of satellite systems to get to the tremendous cash flow we’re producing today. We were profitable on the way but we had to renew ourselves. Now we’ve reached the point where we can pay back investors. Where they’re SPACs or VCs, some investors expect returns in three, five, six, or seven years. They’ve been promised returns in that window, but today, I don’t know of any company in the satellite space that has ever delivered returns in anything less than 15–20 years.

Constellation time horizons are quite a bit different than, say, a SaaS product.

Right, but that doesn’t mean you can’t IPO and certain investors make money or whatever it might be.

How would you explain what it is that you do to the uninitiated analyst or investor? Or even a passerby on the street outside this convention center in Washington? This is a nuanced, complex business—and people may have heard of the flashy constellations like Starlink or Kuiper—but maybe not Iridium.

We were architected many years ago to be extremely efficient at bringing data, which could be voice but also other types of data, to very, very small portable mobile devices, starting with a satellite handset. We’ve scaled down even from there to where we can boil what we do down into the size of a dime.

Is there one in here? [Ed. note: Interviewer wears a Garmin smartwatch and was pointing to it.]

Not yet. But you could connect to a low-Earth orbit satellite through that. From our system, we can deliver not just a broadband connection, but a low-data rate of critical information: where you are, what you’re doing, and what your presence is. If it’s a machine, we can send info about the machine, like pressure or temperature.

That’s all stuff that can be very efficiently sent back and forth between small devices. As for those sexy constellations you just described, they operate in a different frequency band. Returning to the concept of constraints creating innovation, there were not many constraints in KU and K band. They have wide swathes of spectrum.

So what do you do? You say: “Let’s provide the biggest bandwidth pipes we can.” To do that, the physics of wide bandwidth mean you need power and aperture. Short distance helps, but only so much if you’re providing high data rates. The sexy constellations are architected around delivering big pipes.

A lot of people dream that Starlink or Kuiper could disrupt the mobile phone business and create the Tesla super-phone or whatever. But that would be an incredibly inefficient thing to do, architected around giant pipes or delivering that giant pipe to let’s say a watch. That’d mean you were throwing away lots of bandwidth. And they know that. [The LEO megaconstellation players] don’t see us as competitors and we don’t see them as competitors. They go big, we go small.

If memory serves, you’ve referred to those services as “commodity markets” in previous comments. Do I have that right?

I’ve called it “commodity broadband” because they provide a very big pipe that’s not that much different than other pipes. The terminal might be different, but the application is the same. It’s an internet connection, not unlike what you’d get from Fios or Cox. And eventually, I’d expect to see that comparison being made [between LEO and terrestrial broadband].

Iridium has 500 partners who take us to market and have licensed our technology. I believe there’s upwards of 2000 individual solutions tailored to specific use cases: tracking animals, pipeline monitoring, wastewater management, and oil and gas management. It’s specialty broadband, even when we move into higher data speeds. These are safety applications that very critical, featuring just-what-you-need transmissions to very small terminals.

Specialty broadband, among other things, big-a** link-belt excavators.

We most recently brought on Sumitomo, which adds to 6 or 7 of the top-10 heavy equipment manufacturers that are customers. Whether it’s Caterpillar or Komatsu, Doosan or Hitachi, these companies make big pieces of equipment. They’re not just interested in a one-way “Where are they?” They want it two ways: “What’s the oil level? How long has the engine run?” They need to know this for warranty and other purposes, but they also want a connection back into the device to supply information to the driver. They want to know where equipment is not only sold but resold, given the secondary markets for excavators and the like. The manufacturers don’t want to wonder whether they can provide service wherever that machinery ends up.

We went from tracking and two-way monitoring for the largest vehicles, like commercial airplanes and giant ships, down to trucks and heavy equipment. Now, we’re getting down into RVs and personal vehicles. And we’re going even smaller, getting sewn into the uniform of a soldier, being tacked onto a backpack on a hiking trip, or being put in the pocket of somebody. We’ve scaled down really well into those applications where a little bit of critical data going back and forth might be the most important thing for the 85% of the world that doesn’t have cell phone connections.

Like the 80/20 principle for data transmission. Segueing off that, can you explain why IoT is such an important driver for your business?

When the internet started, it was about connecting people at their desks, and then, people on the move. Eventually, we started realizing that machines could be connected with other devices. There were lots of applications that didn’t need people in the loop; that’s what the term IoT is.

Most people know of cellular IoT, like your Ring doorbell or connecting your keys. There are billions of those IoT connections. And while there are really important applications worth connecting to a satellite, there’s not nearly as many. It’s a fraction of the overall IoT market. But these are very important applications that someone needs to track, like shipping containers on an ocean or the flow of energy going through pipelines, windmills, or whatever it might be.

You need to control that process and make it more efficient, which you can do with connectivity. The only way to do that is to get data back and forth. You start with cellular technology, the cheapest way of doing it. But a lot of applications and critical packages go in and out of cellular coverage. Our challenge is making it seamless to go from cellular-based tracking to tracking anywhere on the planet. We’ve done that through devices, back-end partnerships with AWS, and cost-effective payment plans so people can just use the data they need. That business, which has grown at a 20% YoY rate for a long time, is sustaining and long-term, and it drives a lot of revenue.

Where are your cost curves most inflexible? We touched on launch. What about your receivers or terminals? Are there places where you’re not at scale–or high-volume production?

You’re mostly referring to the big mega-constellations in which the business case for an individual, or expectations, are for an internet connection that’s tens of dollars. Those terminals cost thousands of dollars to make. If you’re doing something on the order of millions, getting that terminal down to the $100 or sub-$100 range is out of reach right now. There’s a dream, though: if prices reach those levels, then megaconstellation operators close the business case much more effectively. In our case, we’ve already reached low-cost devices that cost hundreds or tens of dollars.

A mature satellite operator like Iridium is really primarily a fixed-cost business. If you can put the capital into it and bring the system to bear, every incremental second or minute of airtime really falls to your bottom line. If you can just find ways to get people to use your network, it generates profit for you. The challenge, of course, is getting the whole network up there and recovering that cost. That takes time, where the level of business leads to excess cash flow. We’re way past that and now we’re kind of gushing cash.

We have operating margins in excess of 60% right now. Mature companies could be in the 70–80% range.

You know, it’s pretty strange to be talking to a space company that puts up those kind of numbers. Aren’t y’all supposed to lose money?

It’s unusual but really how you should measure any company. Recalling my MBA school days, forget profit and ask: “What’s the cash flow?” Satellite companies are notoriously capex-intensive, and as a result, we tend to say: “Don’t pay attention to capex.” Well, you have to pay attention. At some point you have to pay investors back. We didn’t do that the first time around. $6B was spent on [Iridium’s first-gen] network. It wasn’t going to quickly pay the debt. [Everything] got flushed.

Look at OneWeb—that’s a sexy megaconstellation that unfortunately cleaned its first investors out. And that may happen many more times in this industry. The challenge is getting a sustainable business model with revenues that far outpace capex. There’s a lot of other satellite companies who have large cash flow [but flat growth], so there’s no incentive to provide large multiples. The SESes, Intelsats, are at 6X, 7X, or 8X multiples. We’re much higher than that. We’re not just generating cash, we’re growing, so we deserve a higher multiple.

I’m glad you mention the multiple. I had enterprise value-to-EBITDA ratio on my list of things to ask you about. Using that metric or something else, do you think the market’s valuation of Iridium is fair?

It’s not high enough. Think about the people who look like us, operating data centers or towers. The assets continue to generate lots of cash and the business keeps expanding. Ask an investment banker to screen all the companies like this that have high growth and cash flow. It’s a handful of companies.

Diamonds in the rough.

There are very few of them out there and they’re all very high-multiple companies. I think investors recognize we’re a unique animal right now. We’re not just a satellite company; we’re a satellite company with capex holidays that can generate cash and fully cover capex. We’re not flat with declining revenues and marginal growth. We’re high-growth because we’re doing something quite unique and different, which others can’t do.

I think your challenge, though, and I suppose mine too, is trying to communicate that in the abstract with a nontechnical or non-space savvy audience, no?

The investors who do understand it have been rewarded handsomely for figuring it out. We’re bringing more in. I look for investors who see the long-term growth potential. Beyond the day traders who try to go after whatever’s out, people appreciate that the revenue, cash flow, and five-year fundamentals are why you reward a company like us with a significant multiple.

Space SPACs

What about the multiples of the younger space companies that are newly public, who either have insane 100X multiples or no revenues yet to speak of?

When we went public back in 2009/2010, we did so as a SPAC. We were the only one at the time. There was some redemption, but very little, and no PIPEs. There was a secondary offering but it was a traditional SPAC, at the time. It was very hard to close that, but remember that this happened in the wake of a major global economic meltdown. A SPAC was one of the few options for us, even as a successful business with a 10-year track record of growth. We had a pretty big capex build ahead of us.

It wasn’t like we had to make a new business and prove that it would work. Investors understood, we closed the SPAC, and we got down to business.

These days, due to the excitement of space, I’d say a lot of companies have gone public based on a five-year projection. But they’re built on no track record whatsoever, only future technology and a business idea. They’re suffering now for it, because they’re a public company that still has to invent their business and build from the ground up.

I feel for those companies because they are going to struggle. Space is very hard. It’s literally very unforgiving. It always takes longer than you think, and costs more, and will disappoint you before you ever achieve success. And now, those companies have to go on a quarter-by-quarter basis and apologize for not delivering what they said they would. It’s a horrible place to be.

But it’s a trade-off, right? It’s an easier way to capitalize your business, but one that comes with the baggage of those quarter-by-quarter apologies and other non-trivial downsides.

Yeah. And by the way, I don’t compete with any of those companies. There are a million different business models. I’m a little bit jealous, because it was easier for them to raise money. I wish we had the environment back when we SPAC’d, with the business we had before. But I really do feel for them and wish them the best. I just think they have a long, hard road to success.

It’s pretty crazy to see how redemption rates are trending.

The SPAC sponsors, by the way, made a lot of money. They put their money in and got it out. And some of the early investors have paid themselves off. But now, with a stock trading at half or a quarter of the value, a lot of people got stuck holding the bag.

Switching gears to semiconductor shortages and supply chain issues. You’ve talked a bit about this on recent earnings calls. What’s the latest on that equipment front? Is demand still outstripping supply?

Demand has been extraordinarily high for us since 2020 and 2021. We have significantly more demand than we’ve ever had, right at a time when it’s difficult to expand capacity. Suppliers are limiting what you can get. Fortunately, we’re big enough where we’re getting probably a lot more than what many others, especially startups, can get.

We’ve been able to meet a percentage of our partners’ demand, but stayed behind for the last 12 months. I think we have another 6-12 months before we completely get caught up. We have 500 or so partners, many who I’ve spoken to at the show this week. They know that everyone is in a similar situation, and they appreciate our upfront transparency and tendency to underpromise and overdeliver.

So, we’ve survived so far. We’re not growing quite as fast as we otherwise could but we’re doing okay. I still worry about what I don’t know, but I have a great supply chain team on top of it. We’ve had to pass a little bit of extra cost on to our partners, but not too much. We’re probably eating a little bit of that, but because we’ve had so much demand, it’s sort of lost in our numbers right now.

You make finished products, but also to receivers and chipsets. Don’t you also license the technology to OEMs [original equipment manufacturers]? Has that strategy become more enticing in recent years, given all the supply chain issues?

We believe one reason for our success is our openness to licensing the special sauce to high volume manufacturers who are capable of building us into their products. They can do that in a size and scope we can’t match. Take our general-purpose IoT receiver: A manufacturer could license one part of the receiver and use their own processor and power amplifier.

So, yes, we’ll license. And we’re increasingly moving into air interface (or waveform). Or what you may call software-defined radios. And perhaps you’ll even see us integrating ourselves into general-purpose commercial processing that can go into consumer devices.

We’re open to sharing that. I’m not interested that much in making money on equipment. Even though we make a lot of money on equipment, I really want to create those 60% airtime margins. Actually, it’s higher than that: Our overall airtime margins are ~95%.

SATCOM & Ukraine

What can you tell me about your operations and products in Ukraine?

We’ve kept a low profile but our service has been highly utilized and prized. Our usage has grown by 50X or so, in a short period, and is expanding. This is unlike a lot of natural disasters, where first responders are on the ground, the first three days are critical to peoples’ lives, and bigger comms systems are brought on.

You can’t really do that in Ukraine. It looks like there will be an extended period of time where people really need mobility.

Demand for all of our products there has outstripped supply for all of our products. Satellite phones are obviously the most straightforward product, but there’s also a lot of push-to-talk devices which are really easy to use in these environments. There’s tracking devices and Certus broadband units from our partners. Especially the smaller ones are useful there.

How dialed in are you to folks or organizations within the country?

I can’t believe it. I get at least an email or two a day from a CEO of a humanitarian firm, or a Ukrainian-American firm, trying to find supplies for friends and family, or search and rescue, or refugee operations. It’s been extraordinary.

Via Iridium’s Executive Director, Communications, Jordan Hassin: Thousands of devices have been shipped in. We’ve donated tens of thousands of minutes of airtime to a lot of organizations across the board. Everyone you could think of is looking for this capacity, from one group that wants to rescue orphans to another that is purely focused on refugees.

Back to Desch: And we’ve had doctors, and many, many other types of people using this. But we don’t supply directly. We’re not necessarily shipping product to them ourselves, but we’re trying to make as much product available as we can to the channels that serve those markets. As we get more product, we’re not backfilling empty channels elsewhere. We’re directing it into the channels that can help get product to the people of Ukraine.

I’ve seen reporting that Zelenskyy is using a satphone. I’ve seen speculation—and I want to emphasize that it’s speculation—that he’s using one an Iridium handset. Is Zelenskyy using one of your satphones?

I will be honest: I don’t know. I really don’t know.

That’s typical in a lot of cases. There’s not many other secure satellite phones, but perhaps the DoD does have some of their own systems. And there are other tactical radio systems that could work. I would love to allude that it’s necessarily ours [but can’t say for sure]. It is not an unusual use of our service.

If it is us, it seems to be working very well for him and I hope he continues to use it to great effect.

Well, he’s had pretty solid opsec and clearly isn’t incommunicado. I suppose it’s no surprise that among the very few folks who make these systems, nobody can (or will) say for sure.

Via Hassin: If it is our phone, then he’s using a secure DoD/governmental gateway.

Back to Desch: Yeah, they have their own, if it’s a secure phone. That’s one of the reason why the DoD is 20% of our business. They have a private network on our otherwise public network. They’ve encrypted all of their communications and it doesn’t touch ground.

There’s nothing in that area where the service comes down in a bent pipe situation into a ground gateway. Our fast-moving satellites in LEO aren’t not easily jammable. It’s difficult to impede the service, which is why it’s relied upon by so many people.

It’s pretty surreal seeing topics like GEO jamming play out in real time. On the topic of dual-use, could you say a bit more about your government/military-facing business?

We’ve had a 25+ year relationship with the DoD. First of all, I’d say they like our network because it’s operationally secure. We don’t see where they’re using the devices and have no operational picture into what they’re doing. Not true of other opportunities they may have.

One of the biggest benefits over time for us has been situations where they have a specific application they want to build. Often, we’re able to then utilize that for commercial customers.

For example, the DoD wanted a tactical radio that would work as a net anywhere on the planet. They had no service like that, that was so broad-based. It was called a distributed tactical communication system (or DTCS). They put some money into it. We were quite small at the time and didn’t have the R&D funds to do it alone. But working with them and some partners, we built a system to assign resources in real-time for multiple users, first in a beam, then across multiple beams, and then across multiple satellites. It’s a very powerful capability that nobody else has.

At some point, DoD started using it less. We realized the service was something that commercial customers would love. Now, it’s one of our most popular services. You could literally have a net of people across South America, North America, Europe, and Asia that push a button and all hear the same thing. You can imagine how important that has been in natural disasters of all sorts. Americans have one, the person at the airport has one, the person on the rescue boat has one.

And it’s about 20% of your business? Do you see that share, between commercial and USG, changing over time?

Our commercial business is growing far faster than our government subscribers, who make up a fraction of our subscribers and ~20% of our revenue. We’re used by all kinds of governments and state departments. We track embassy workers when they’re out of their embassies in bad places. We’re used by the Energy Department, firefighting organizations, the Coast Guard, intelligence agencies, and special ops forces, obviously. Not even just for tactical reasons, but morale, too. Soldiers can call home. A wounded soldier on the field can talk to their family. A lot of soldiers got to know us because they were able to use us in critical times. And they become long-term commercial users after they retire.

ELI5 & a Few More Rapid-Fire Questions

Explain it to me like I’m five: What’s the value of the L band?

A lot of people don’t appreciate that they’re just letters that were assigned many, many years ago by the ITU. The L band is fairly close to cellular frequencies. It’s anywhere between ~1.5 and ~2.5 gigahertz. That’s very much exactly where cellphones radiate, within that general area. There are special satellite bands that are really designed for satellites, and which were allocated many years ago to a number of companies back in the ‘90s and 2000s to support service.

Because the L band frequencies’ waves are longer, then say, the microwave frequencies like KU and KA band, where bands are very short, they go through rain, wood, and materials easier. They’re not easily blocked by bad weather and whatnot. And because they are longer, actually the antennas can be smaller. In L band, the antenna for a satellite phone is actually only the size of the end of your thumb.

So it’s easier to capture signals?

It’s the perfect mix of propagation characteristics and speed. Actually, another advantage is the chips in electronic products that are made for cellular phones. They’re very close in capability, along with GPS, which means antennas can be quite cost-effective.

You can take advantage of the economies of scale that come with manufacturing billions of smartphones.

Yeah. You can get components, like power and amplifiers, that were built for a mass market. Many other satellite markets are in quite specialty areas. Right now, people are talking about going up to the V band, which is really up there. There’s a lot of spectrum but there are no components that have been built for that band. It’s going to be very expensive for a long time. ents that have been built for V band. It’s going to be very expensive for a long time.

As we’re pushing up on time, I’ll pull another random question from my grabbag. Tell me about your threat landscape, especially in light of current geopolitical tensions.

Our wake-up call was about 12 years ago. Based upon the Russian and Chinese ASAT tests—and hackers we saw trying to penetrate our network—we saw that space networks were going to be front and center targets in warfare, global commerce, and communications. We’ve spent a lot of money and time working to protect ourselves, educate our workforce, and take precautions that we think make sense. And we never get satisfied or comfortable. I appreciate the CISA Shields Up memo. Another wake-up call is the Viasat modem situation. But it really isn’t anything new to us. It doesn’t increase my paranoia, which is already high enough as it is, when it comes to cybersecurity. It’s sorta business as usual for us: We’ll keep doing what we’re doing, hiring people do break into our network, analyzing our architecture, and moving fully zero-trust.

Any M&A on the horizon?

I get asked that a lot because of our cash. We have three investments right now: 1) Aireon, an aircraft-tracking service, 2) Satellus, an alternate PNT service, and 3) DDK Positioning, a GNSS precise-point-positioning service. I see us investing more in them to ensure their continued success. We are talking to people about ideas, but have no need to go outside of our lane. If there was something that was right in-line with our mission, I’d be open to it. But we’re not shopping, per se.

Final question: The iPhone rumors from last year—a nothingburger? [Note: this refers to a Aug. ‘20 Bloomberg report that a future iPhone model could contain a satellite interface.]

Well, let’s just say Iridium in a smartphone. Absolutely [that’s a possibility]. I’ve been saying for the last year that the Apple rumor was a wake-up call to the industry about a satellite interface being integrated into a small device. There’s very few companies that can do that. We’re one of them. We believe our network was built perfectly for something like that: a future where we’re connected to consumer devices of all types. Smartphones are one [form factor], but it could also be wearables, autonomous vehicles, small drones, and RVs. We really believe we shouldn’t be in the ~2M devices we’re in today, but hundreds of millions of devices down the road.

NASA Releases CLD Draft RFP

NASA is officially moving forward with its original plan to support stand-alone replacements to the ISS, after industry proved its take on human habitation in LEO.

Exclusive: Satellogic Expands AI Apps with SpaceKnow Partnership

Satellogic partnered with SpaceKnow, the AI-powered geospatial intelligence analysis company, to build AI applications on top of Satellogic’s growing stock of satellite imagery.

Exclusive: SpaceComputer and Spacemanic Partner on Security Demo Mission

Space Fabric is SpaceComputer’s solution not only for the growing hacking threats on-orbit, but also for the increasing number of shared-compute modules operating on rideshare sats.

Japan Eyes Sovereign D2D Satellite Network

Japan plans to select a proposal this month for its domestically owned and operated D2D satellite network, called J-LEO.

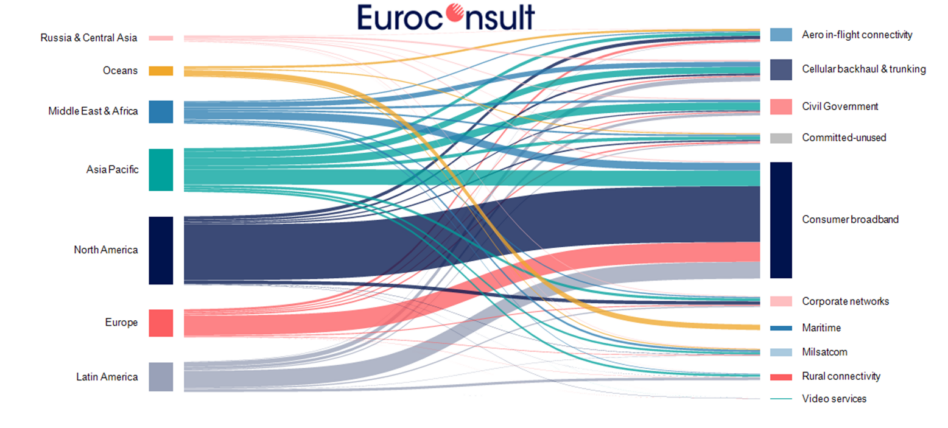

Projected HTS capacity demand in 2030. Graphic: Euroconsult

Euroconsult has released the 6th edition of its report on the High Throughput Satellite (HTS) market. The takeaway: Business is booming. The HTS market has seen major growth since 2019, and that growth is expected to continue booming over the next few years.

Euroconsult predicts growth in nine key areas:

Keep reading