Research

Insights and analysis from Payload Research

NASA Releases Updated Software Catalog

NASA is continuing its tradition of not gatekeeping success by unveiling a major update to its public software catalog.

Direct-to-Cell Pricing Revealed, Market Impact: Analysis

The most exciting moment of Sunday’s Super Bowl was finally getting concrete direct-to-cell pricing numbers.

Tracking US Mobile Satellite Service Spectrum

The MSS landscape is about to evolve rapidly as incumbents form new partnerships to ride the D2D wave while new entrants work to get access to the valuable MSS spectrum.

Estimating SpaceX’s 2024 Revenue

Payload is back with our SpaceX revenue breakdown. In 2024, we estimate SpaceX’s revenue reached $13.1B in 2024, up from $8.7B in 2023. Business line estimates:

US Launches 122 Defense Payloads in 2024, Europe Launches 1

The US launched 122 defense payloads in 2024, surging 184% YoY, according to data compiled by astronomer Jonathan McDowell. The upswing was driven by the National Reconnaissance Office’s deployment of 106 SpaceX and Northrop-built Starshield remote sensing recon satellites.

Underutilized Capacity on Dedicated Customer Falcon 9 Rides: Payload Research

Based on publicly available data from 20 launches with published payload mass numbers over the past three years, dedicated customer LEO launches have averaged just 3,370 kg of payload, just 19% of total capacity.

NGSO Fixed Satellite Service Spectrum Priority in the US: Payload Research

Last month, the Federal Communications Commission (FCC) updated its spectrum sharing rules for Non-Geostationary (NGSO) Fixed Satellite Service (FSS) systems to establish quantified interference protection criteria for satellite systems based on their level of spectrum priority.

Tracking Cash Flow Through the 2024 Space Stocks Rally

Hockeystick SPAC charts. Wallstreetbets Reddit page buzz. Short squeezes. Everything to the Moon euphoria.

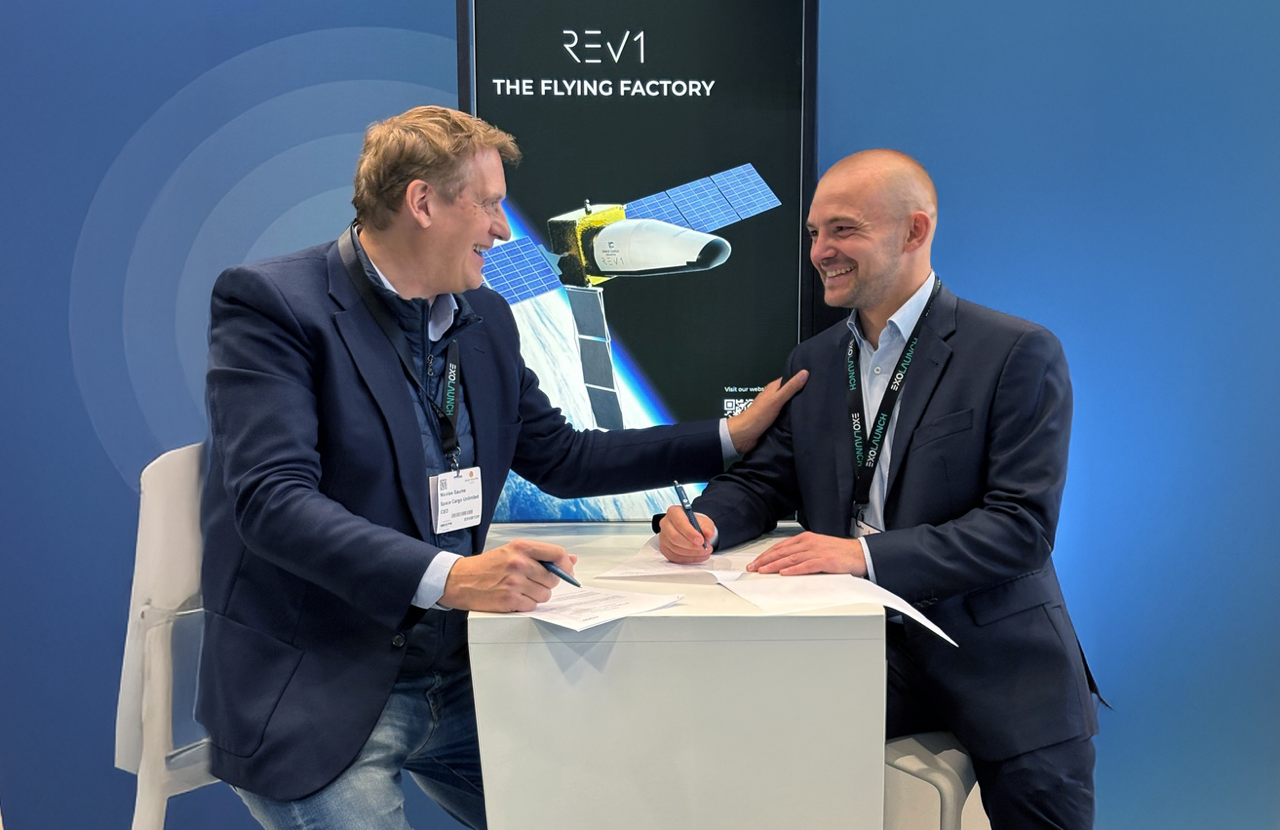

European Space Cargo Start-Ups Strike Seven Mission Deal

Germany’s ATMOS Space Cargo and France’s Space Cargo Unlimited (SCU) are teaming up.

Startups Race to Make Space-Based Power a Reality

In this article, we will review four companies pioneering space-based solar power, and their different approaches.

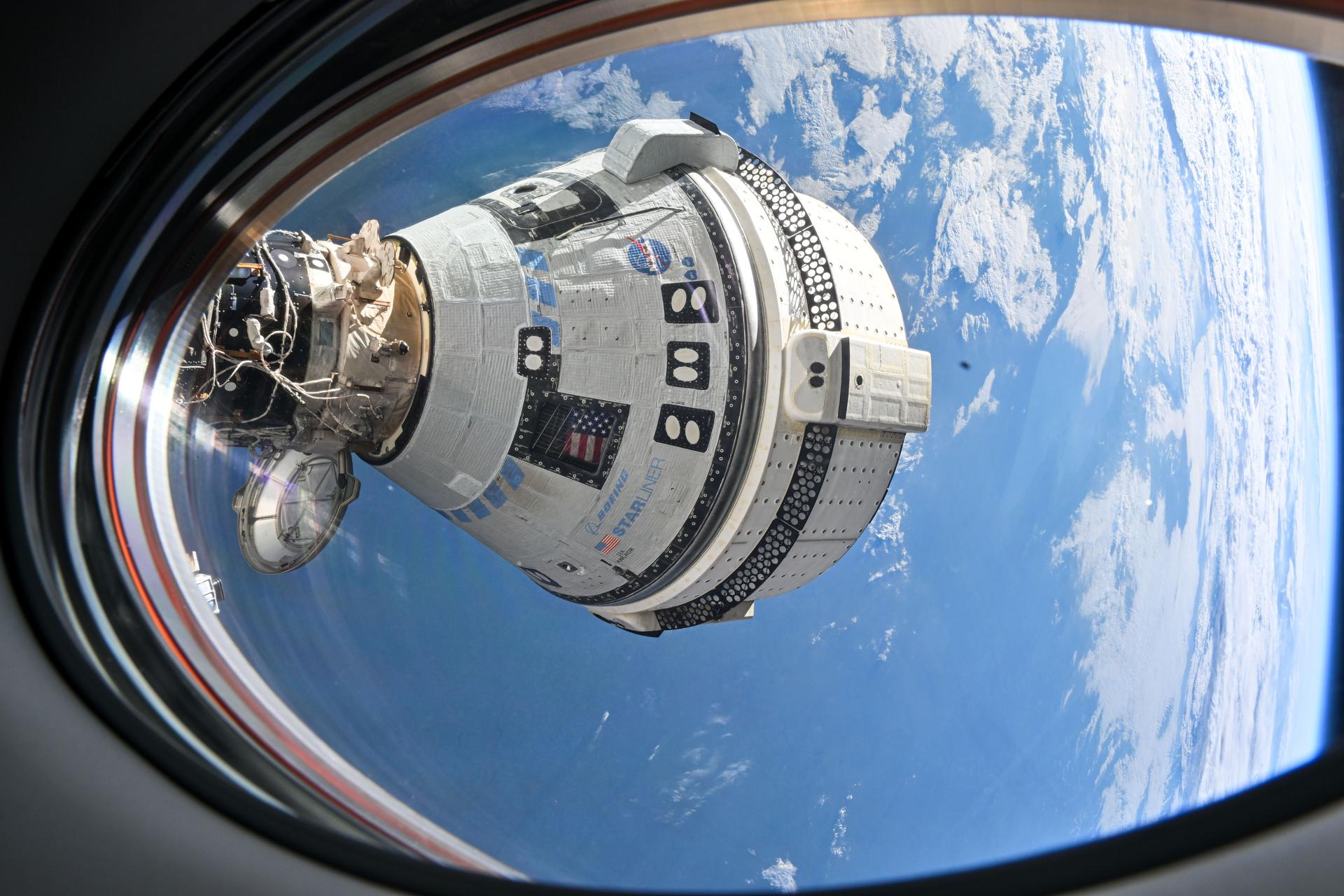

The Starliner Investment Case and Potential Buyers: Payload Research

First, a ULA sale process, now Starliner.

Comtech Looks to Sell Half its Business, Go All-in on Space

Comtech ($CMTL) announced last week that it is looking to sell its terrestrial 911 emergency call infrastructure business to go all-in on space comms.