Comtech ($CMTL) announced last week that it is looking to sell its terrestrial 911 emergency call infrastructure business to go all-in on space comms.

The Board of Directors said the company is “in the midst of a transformational journey,” and proceeds from the potential sale will help rightsize its balance sheet.

A bit lopsided: In Q3, the company reported $128M of revenue, a 6% YoY decline. Comtech carries ~$160M of debt, $27M of cash on hand, and a tiny $109M market cap, down over 50% YTD.

Tough times call for tough measures. For management, that means offloading their faster-growing, higher-margin, and more valuable business line.

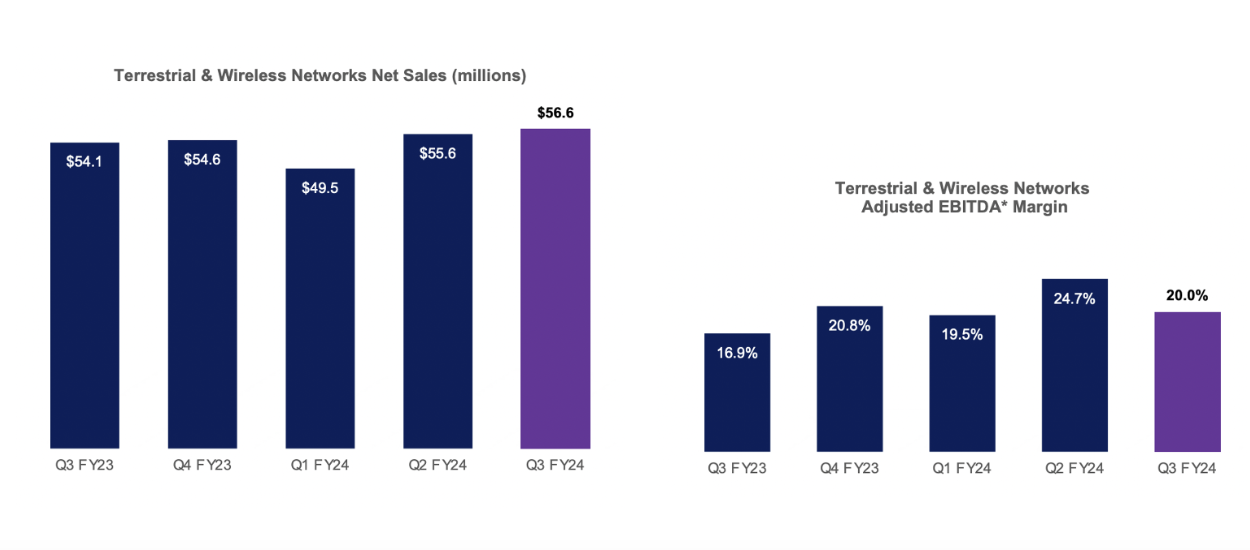

Goodbye, Next Generation 911 (NG911) terrestrial emergency calling:

- NG911 is an upgraded emergency response system that allows people to connect from more devices via voice, text, or video. A July FCC ruling established a new framework that could help speed up the nationwide adoption of NG911.

- The division generated $56.6M of Q3 revenue, supporting a strong $11.3M Adjusted EBITDA.

- The segment doubled its booking this year, including a $140M Massachusetts contract renewal.

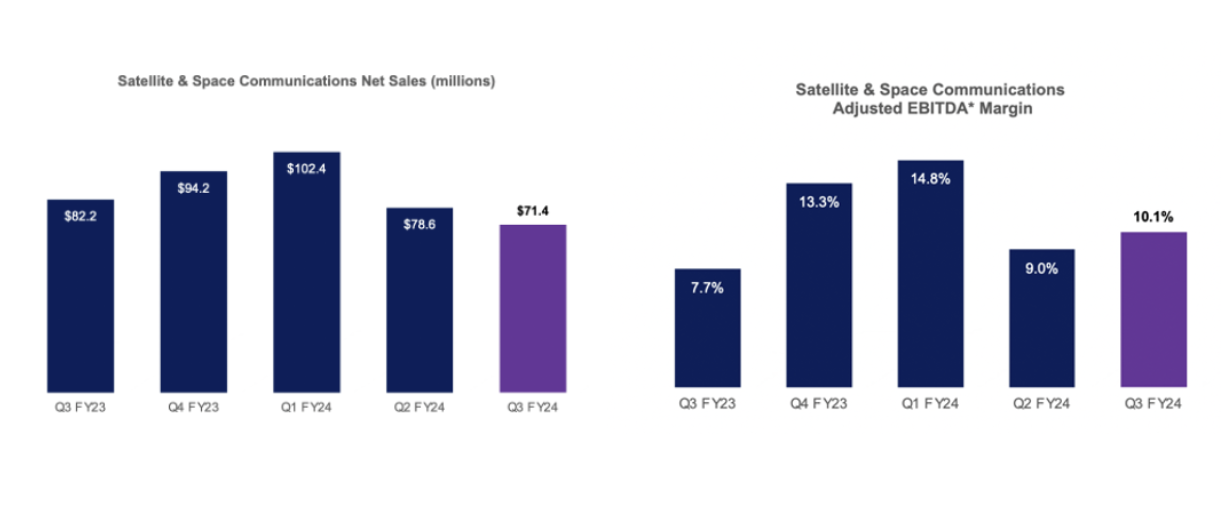

Satcom business:

- The company’s satcom products include modems, signal-boosting amplifiers, and troposcatter tech.

- The segment primarily serves the DoD and large defense contractors, providing connectivity and coordination to warfighters across branches—a focus area for the military.

- With rising geopolitical tensions and defense spending, the company views the business as ripe for growth, despite declining quarterly sales.

- In Q3, the division generated $71.4M of sales, down both YoY and QoQ.

Debt, debt, debt: In addition to exploring the possibility of divesting nearly half its business, Comtech also announced last week it raised an additional $25M of high-yield subordinate debt—adding to the company’s debt burden until a sale can be completed.

The company has struggled with its debt overload for quite some time now, having recently closed a $222M credit facility in June to refinance debt that was coming due in October.

With a market cap of just over $100M, the company is in survival mode to ward off the banks.

Its 911 emergency infrastructure business generates a healthy ~$40M in annual Adjusted EBITDA. A sale of the division could return a pretty penny, taking care of that pesky debt problem. The company is also exiting a UK subsidiary this year, which they expect will net ~$10M of annual cash savings.

The move coincides with a challenging period for publicly traded space stocks. As cash reserves shrink, public markets become less inclined to provide funding, and management increasingly mentions “seeking strategic alternatives.”

Exclusive: Satellogic Expands AI Apps with SpaceKnow Partnership

Satellogic partnered with SpaceKnow, the AI-powered geospatial intelligence analysis company, to build AI applications on top of Satellogic’s growing stock of satellite imagery.

Rocket Lab Enters the Satcom Market With $8B Iridium Deal

Rocket Lab ($RKLB) has been teasing its entrance into the “space applications” market for years. Yesterday, it pulled the trigger.

SpaceX Alum Have Raised $9.2B, New Data Shows

As an organization that’s employed thousands of engineers in its 24-year history, SpaceX has acted as both a breeding ground for high-level engineering talent, and as a launch pad for new ideas.

Firefly Acquires Autonomous Space Ops Company

Firefly Aerospace announced yesterday that it acquired Space-ng, which is an AI-powered vision navigation and autonomous guidance systems provider.

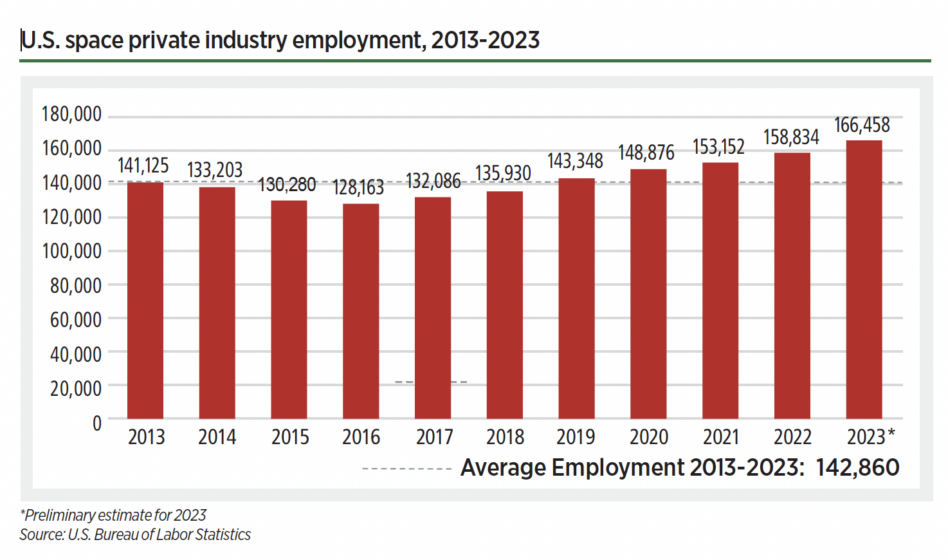

The space industry is getting crowded.

The sector added 26,000+ jobs between 2022 and 2023 in the space heavy-hitters, including the US, Japan, India, and Europe, according to a new report from Space Foundation.

This growth is about four times larger than the number of workers added a year prior and points to a thriving global space economy that has nearly doubled in size over the past decade.

Keep reading