The worst-kept secret in the space industry is coming to a head.

ULA is up for sale, and all signs point to Blue Origin as the buyer. While the two parties have not yet signed an agreement, a deal for ULA—which Boeing and Lockheed formed as a joint venture in 2006—could be announced in the next couple of months, Ars Technica first reported. Our sources confirm that the sale should be announced by the end of April. The valuation for ULA is thought to be in the $2B to $3B range—and could be as high as $4B.

Jeff Bezos is all-in on Blue Origin. Over the last decade, Blue has invested heavily in the development of its next-gen heavy-lift New Glenn rocket, culminating in the vehicle’s first rollout to the pad last week. With Bezos’s eyes now set on ULA, he has been on an Amazon stock-selling tear, cashing out $8.5B worth of shares (representing just 5% of his total holdings) in recent weeks.

Why would Blue Origin want to buy ULA? ULA is a legacy launch business, building expendable rockets, and banking on an unproven Vulcan rocket, while Blue is laser-focused on developing its cutting-edge 45-ton-to-LEO reusable New Glenn rocket.

Here is the investment case.

ULA Business Strengths

- Vulcan maiden launch: ULA nailed Vulcan’s January maiden launch. Vulcan is ULA’s next-generation expendable vehicle, set to replace the company’s legacy rockets.

- R&D: The years of heavy Vulcan R&D investment are now behind ULA and are starting to pay dividends.

- Strong projected Vulcan ramp: The company aims to launch Vulcan six times in 2024–-ramping up its booster production rate to 25 a year by late 2025.

- Kuiper contracts: ULA has sold over 70 Vulcan launches, including 38 Amazon Kuiper missions.

- NSSL contracts: The company has 26 Space Force’s National Security Space Launch (NSSL) Phase 2 launches on the books, highlighting its strong relationship with the Pentagon.

- The national security missions are valued at ~$118M, representing roughly $3B in backlog.

- Proven track record: ULA has an experienced workforce, leadership, and a successful launch history.

ULA Business Risks

- Reusability: Vulcan is not reusable—although designs are underway to eject its BE-4 engines post-launch and recover them via an inflatable heat shield and parachute.

- Competition: Vulcan competes with SpaceX’s Falcon 9.

- Vulcan question mark: Vulcan hardware is unproven.

Pace of innovation: ULA has been historically less aggressive in pushing technological boundaries.

Market Data Points

- Aerojet bid $2B to acquire ULA In 2015.

- L3Harris bought Aerojet for $4.7B last year.

- Rocket Lab’s current market cap sits at $2.3B.

- According to Boeing’s 2023 10-K, the company values its ULA equity investment at $582M, down from $771M in 2019.

- Considering the company’s 50% equity stake, Boeing’s implied ULA valuation is $1.2B.

- ULA’s profitability is declining.

- ULA’s profitability has seen a decline from a peak of ~$650M in 2016 to ~$80M in 2023 primarily due to the Vulcan transition and share loss to SpaceX.

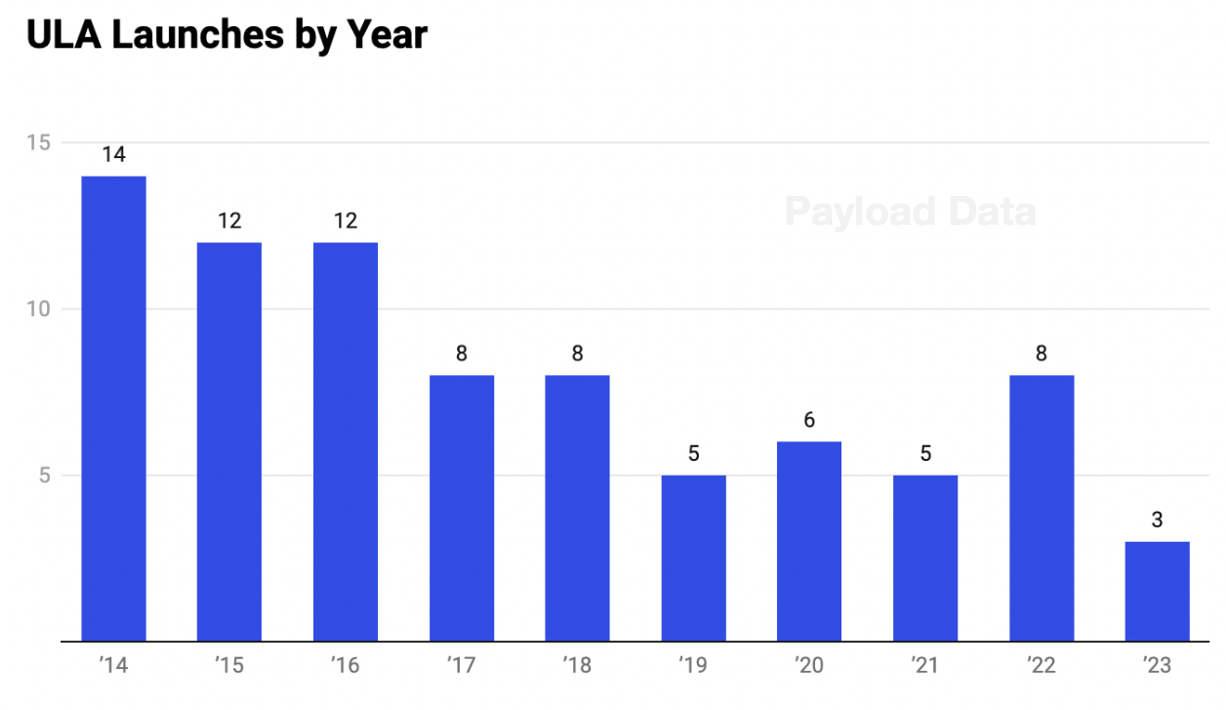

In 2015, ULA introduced Vulcan as its next-gen launch vehicle that would replace the Atlas V and Delta IV rockets. That same year, SpaceX landed a Falcon 9 booster for the first time, setting the stage for a decade of high-cadence launch dominance. With Vulcan slated for a steep ramp over the next few years, ULA’s launch rate is poised to increase substantially.

Blue Origin’s ULA Investment Case

Value is in the eye of the beholder: ULA offers greater value to Blue Origin than to private equity investors or as a standalone operation. Let’s dive into why Blue Origin would want to buy ULA.

- Inherited contracts: ULA’s existing contract backlog provides immediate market penetration and revenue. ULA’s launch backlog (possibly over $7B) far exceeds what Blue will pay for the acquisition.

- BE-4 synergies: Blue Origin supplies ULA with the BE-4 engines that power Vulcan. Tucking Vulcan into Blue’s portfolio immediately creates millions of dollars of synergies per rocket.

- Consolidating market: Acquiring ULA removes a potential competitor, consolidating Blue Origin’s position in the market.

- Leadership: ULA chief Tory Bruno is a respected leader. His engineering background could complement Blue Origin’s newly appointed CEO Dave Limp, a former Amazon executive who has strong management experience.

- 20-ton-to-LEO capability: New Glenn is a heavy-lift reusable launch vehicle capable of carrying a staggering 45,000 kg to LEO. However, current satellite designs generally don’t require that much capability. For example, SpaceX’s Falcon 9 (18 metric tons to LEO reusable) attracts significantly more demand than its much larger Falcon Heavy counterpart. Vulcan would allow Blue Origin to compete in the medium-lift launch market.

- Footing the bill: The reported $2B-$4B acquisition cost, while substantial, is relatively modest compared to Blue Origin’s bills.

- Blue Origin’s yearly expenses: Blue Origin employs 11,000 people (!), just shy of SpaceX’s payroll of 13,000 employees. If we assume an average employee salary/benefits cost of $150,000 per year, it would mean Blue spends ~$1.7B a year on its people alone. Add in facilities, materials, construction, and development costs, and Blue Origin’s yearly expenses could easily exceed the cost of buying ULA.

Investment question marks:

- Vision: ULA is a legacy launch provider building expendable rockets, contrasting Blue Origin’s ambitious reusability goals.

- Regulatory dynamics: Since the acquisition would consolidate the market, it could face regulatory pushback. The government would like to see more diversity and competition in launch providers, not less.

Boeing and Lockheed divestiture rationale: Selling ULA allows Boeing to focus on its core businesses and address 737 Max challenges. Moreover, the launch landscape is growing markedly more competitive, with a substantial increase in capacity (Starship, Ariane 6, Neutron, New Glenn, Antares 330, Terran R) expected to come online over the next few years.

Broader Industry Impact

National Security Space Launch Phase 3 awards, which are expected to be announced later this year, could open the door for a third launch vehicle *ahem New Glenn* for national security launches. The acquisition could influence the competitive landscape for these launches.

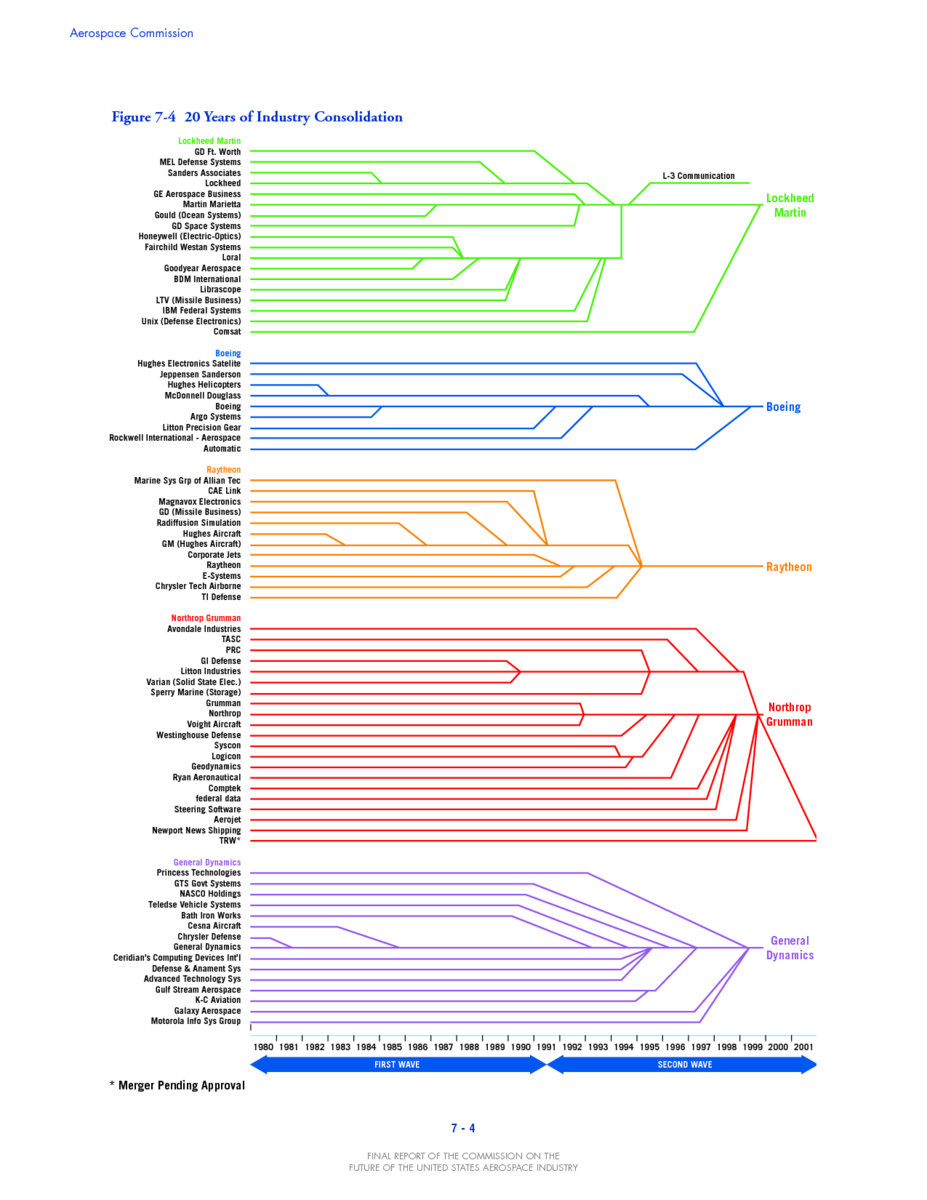

Rocket consolidation: The chart below is a favorite amongst the Payload team. Like the A&D consolidation in the ’80s and ’90s, which resulted in just a handful of prime contractors and two major commercial plane manufacturers (after Boeing acquired McDonnell Douglas), Blue Origin’s potential ULA acquisition consolidates the market into fewer but better-funded players.

Image: 2002 Commission on the Future of the United Space Aerospace Industry

NASA Releases Updated Software Catalog

NASA is continuing its tradition of not gatekeeping success by unveiling a major update to its public software catalog.

Direct-to-Cell Pricing Revealed, Market Impact: Analysis

The most exciting moment of Sunday’s Super Bowl was finally getting concrete direct-to-cell pricing numbers.

Tracking US Mobile Satellite Service Spectrum

The MSS landscape is about to evolve rapidly as incumbents form new partnerships to ride the D2D wave while new entrants work to get access to the valuable MSS spectrum.

Estimating SpaceX’s 2024 Revenue

Payload is back with our SpaceX revenue breakdown. In 2024, we estimate SpaceX’s revenue reached $13.1B in 2024, up from $8.7B in 2023. Business line estimates:

Rocket Lab Needs Neutron

The second-busiest US launcher’s losses—and future profits—all hinge on Neutron, a rocket designed to compete with SpaceX’s Falcon 9.

CEO Peter Beck said the first hot fires of the new Archimedes engine will set the schedule for the rocket, which the company has ambitiously forecast to be on the launchpad this year.

Keep reading