The space industry is preparing to send tens of thousands of satellites to orbit in the coming decade, building out large constellations across the spectrum of possible capabilities. They may run into a bottleneck, however, when it comes to booking tickets to space.

This morning, McKinsey released its analysis of the demand for launch services compared with the supply of launch services. The analysts found that as more startups prepare to launch their first satellites and expand their growing constellations, there is still a significant shortfall in the near term in the supply of medium- and heavy-lift launch services.

Supply and demand

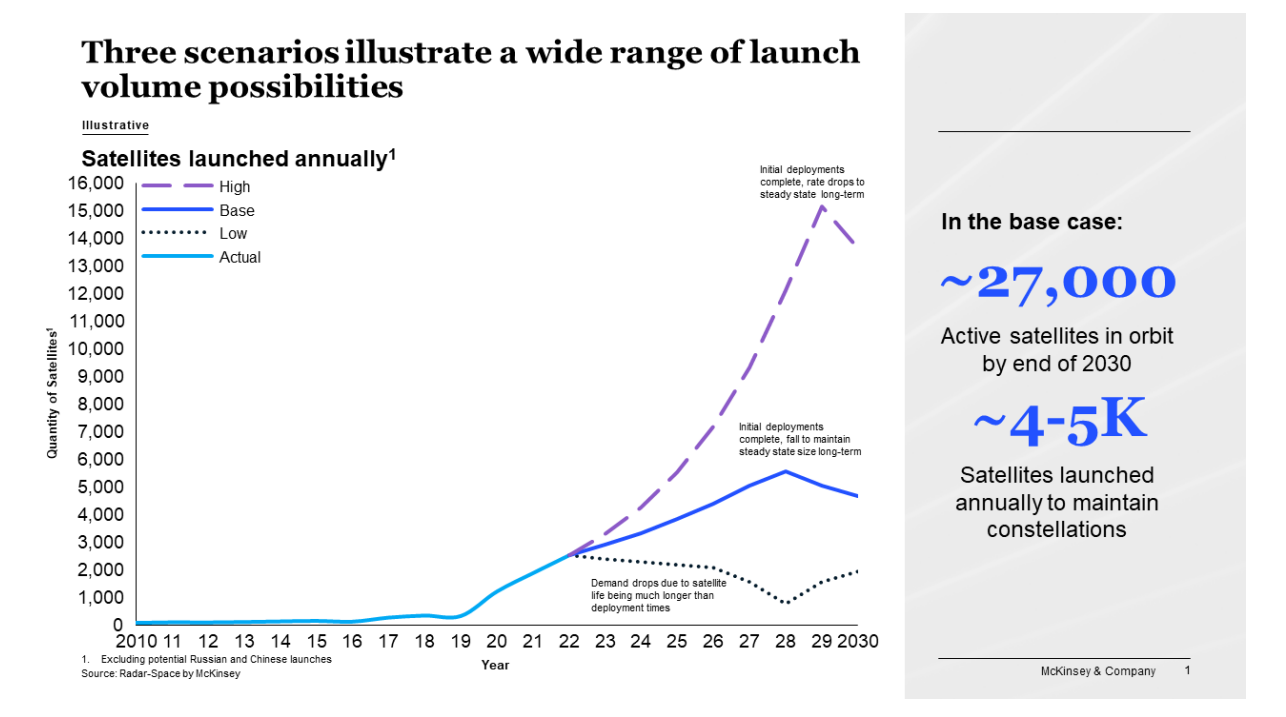

Right now, the McKinsey team tallies ~7,500 satellites orbiting the Earth. ~5,000 of these are used for comms, ~1,000 for EO applications, and ~1,500 for tech dev and research purposes.

- Looking ahead, the analysts found demand to launch up to 67,000 more with an average mass of 1 ton, largely dominated by communications sats.

- The base case is a little more modest, showing 24,000 new satellites are likely to be deployed by 2030 with an average mass of 870 kg.

The Starship effect: The bull case hinges on Starship’s success. If the mega-rocket is able to reach the launch cadence it promises—a daily launch rate by 2030 and a fleet of 30 boosters and 60 ships—then the analysts see more than double the launch capacity for the industry than in its base case.

On supply: “While demand dynamics are uncertain, launch is also at a tipping point,” the analysts wrote. “Many medium- and heavy-launch vehicles are being retired, and most remaining capacity is already booked.”

ULA’s Atlas V, Arianespace’s Ariane 5, Mitsubishi Heavy Industries’ H2, and Northrop’s Antares 230+ are nearing the end of their lifetimes, leaving a medium- and heavy-lift gap in their wake. For the foreseeable future, McKinsey writes, SpaceX will continue to dominate access to orbit with the Falcon 9 and Falcon Heavy.

Several new rockets—including the Ariane 6 and New Glenn, besides Starship—are scheduled to come online soon, but the gap in capacity doesn’t have a quick-fix solution.

“Of course, in space commerce, there is often a yawning gap between intention and execution,” the analysts write. “A rocket in development is not equivalent to being able to offer an immediate or scheduled ride into orbit. In all cases, we expect a significant ramp-up period, even after a successful first flight.”

Assessing the impact

In the short term, the McKinsey analysts doubt that companies with ambitious timelines to deploy large constellations will be able to meet their targets. In the long term, though, demand is expected to stagnate while launch supply continues to increase—meaning launch providers will have to prioritize cost control and reliability from the beginning to ensure competitiveness in the long term.

“The data, in aggregate, suggest that the space industry faces a potential double bind,” the analysts write. “In the short term, the most likely scenario is a capacity shortfall, but in the longer term, the biggest risk is oversupply.”

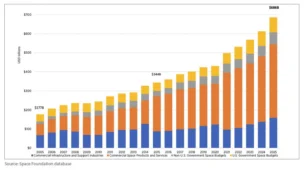

Breaking Down the $686B Space Economy

The global space economy totaled a record $686B in 2025, according to the Space Foundation.

Skyroot Aerospace Reaches Orbit with Vikram-1 Rocket

Skyroot Aerospace became the first private Indian company to reach orbit on Saturday, when its Vikram-1 rocket lifted off from India’s primary spaceport—the Satish Dhawan Space Centre.

DoD Adds $11.4B to NatSec Launch Contracts

The DoD upped its ceiling for national security space launches on Friday, more than tripling the pool of NSSL launch contracts from $5.6B to $17B.

Spinifex Space Launches With Australian Test Ranges

Spinifex Space will provide end-to-end suborbital launch campaigns, private range access, and test and evaluation (T&E) infrastructure.

Happy belated Transporter launch day to all who celebrate.

At 2:48am Saturday, SpaceX launched the Transporter-7 mission on a Falcon 9, carrying 51 customer payloads to new homes in orbit.

These rideshare missions are big days for small satellite companies that rely on the comparatively low cost to send their birds to orbit. On this flight, SpaceX safely delivered batches of EO satellites, sensors, OTVs, and precious cargo for first-time fliers. Here’s our highlight reel and recap of the riders on the mission.

Keep reading