Ed. note: This is Payload Research analysis. You can sign up for our Research newsletter here.

The first three months of 2024 was another busy quarter for the space industry, underscored by continued growth in SpaceX’s launch cadence and a solid VC funding environment. Below are the four charts defining the quarter.

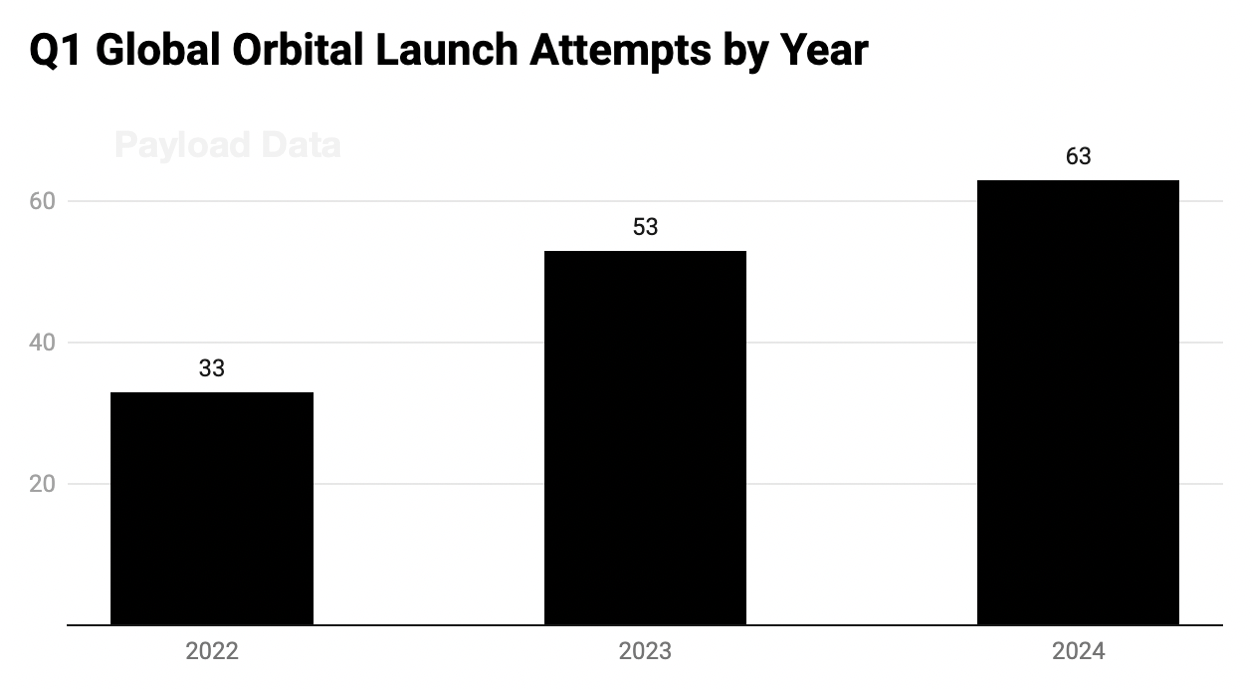

The total number of global orbital launch attempts in Q1 increased by 10 missions in 2024, a 19% year-over-year increase. The growth can be attributed to SpaceX, which saw an increase of 11 launches in Q1 2024 vs. Q1 2023.

More capacity is on the horizon with Vulcan, Starship, New Glenn, and a host of Chinese launch startups set to increase launch cadence over the next year.

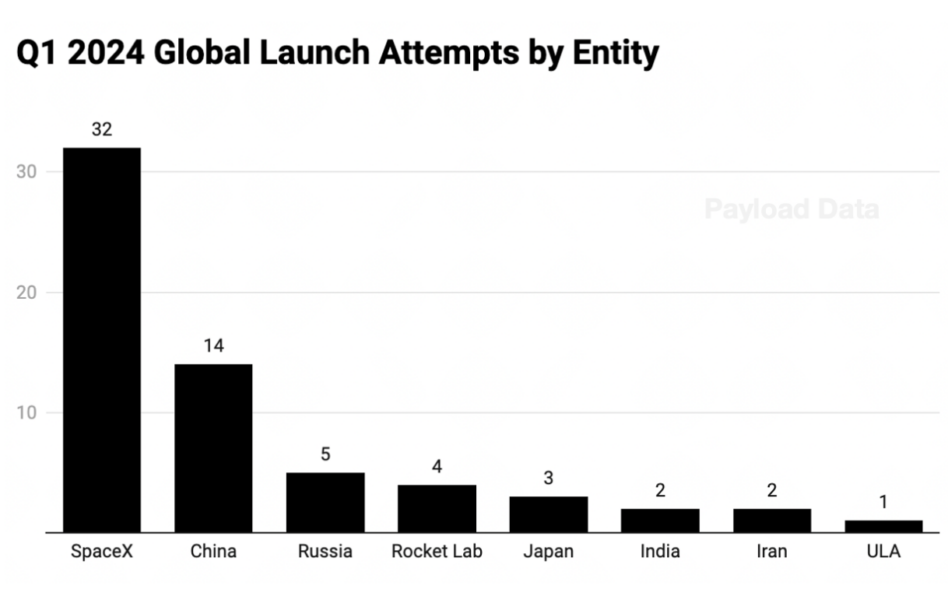

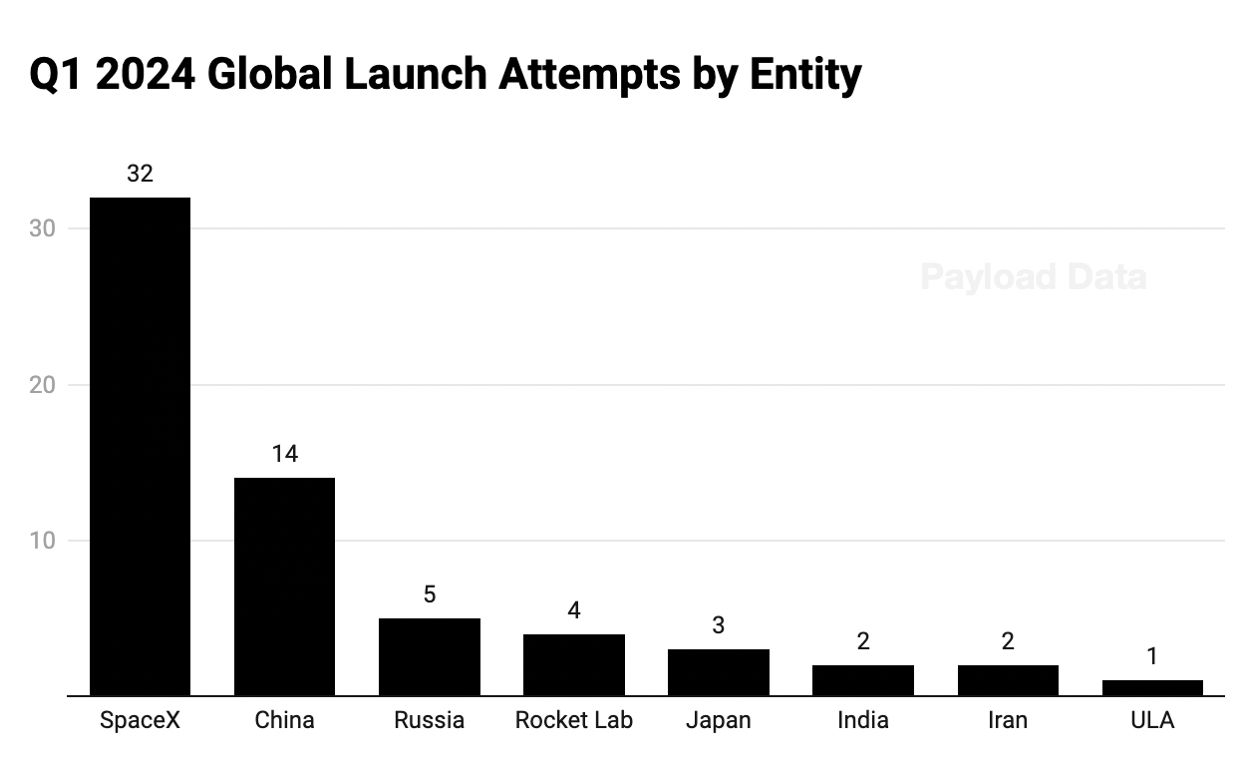

Key takeaways:

- With a gap between Ariane 5’s retirement and Ariane 6’s debut, Europe registered zero launches last quarter.

- Iran launched two rockets in Q1 compared to one in 2022 and two in 2023.

- Rocket Lab launched four times in Q1 as it looks to build off the nine missions in FY23.

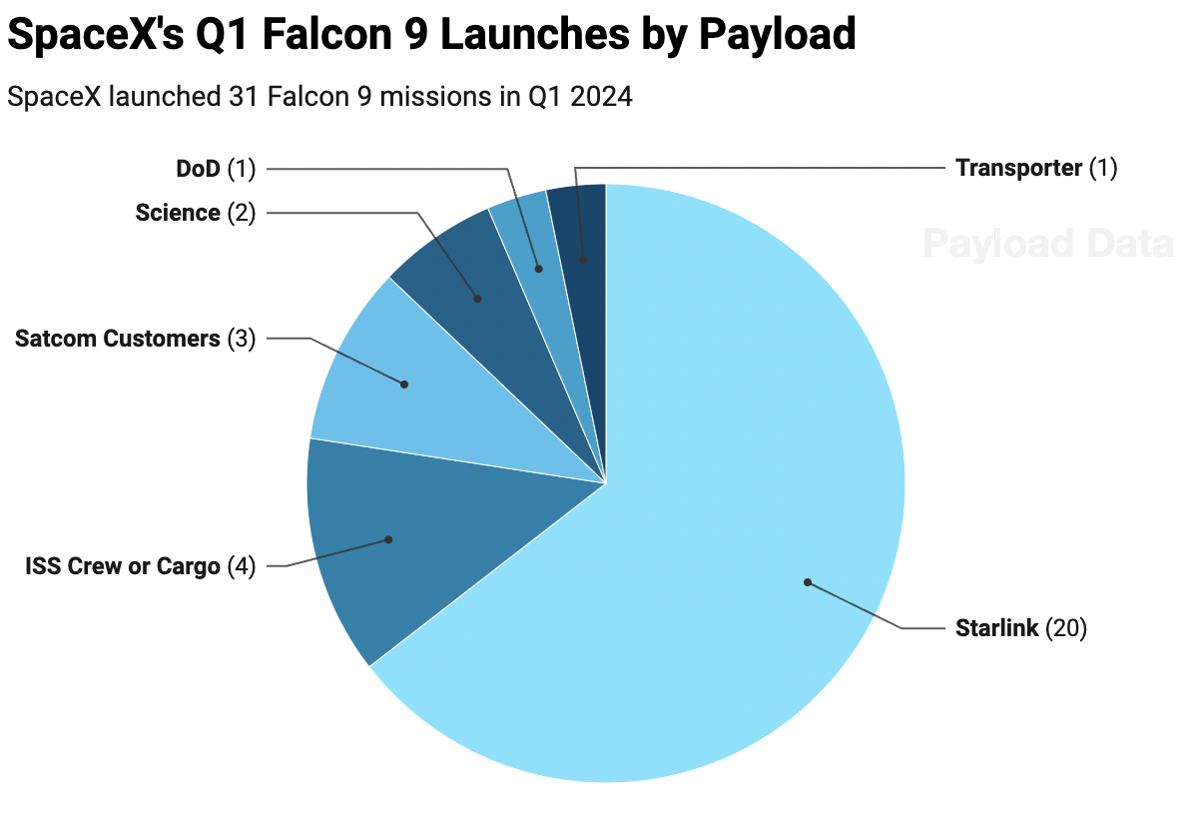

- SpaceX’s launch count includes 31 Falcon 9 launches and one Starship launch in 2024.

SpaceX launched 31 Falcon 9 missions in Q1, matching the total number of launches the company recorded in 2021.

The pace of launch is increasing month over month, with SpaceX hitting 12 Falcon launches in March.

Falcon launches by month:

- January: 10

- February: 9

- March: 12

Still, based on its Q1 pace, the launch giant is ~15% behind its goal of 148 Falcon launches. To hit that target, SpaceX will need to average 13 Falcon launches per month for the rest of the year.

The Q1 payload breakdown:

- 1 DoD: SpaceX launched USSF-124, which included four SDA Tranche 0 tracking layer birds and 2 HBTSS. Falcon 9 also delivered two Starshield satellites as a secondary payload on a Starlink flight.

- 1 Transporter mission: Falcon 9 hosted 53 customer payloads on Transporter-10.

- 2 science: SpaceX’s Q1 science missions include NASA’s PACE ocean monitoring bird and Intuitive Machines’ IM-1 lunar landing mission.

- 3 customer satcom: SpaceX launched Telkomsat’s Merah Putih 2 satellite, Eutelsat 36D, and Ovzon-3.

- 4 ISS missions: SpaceX launched four missions to the ISS last quarter. Crew-8, Ax-3 private crewed mission, a Northrop Grumman Cygnus cargo resupply mission, and a Dragon resupply mission.

- 20 Starlink missions: Starlink continues to dominate Falcon launches as SpaceX looks to rapidly deploy its constellation and boost capacity. This year’s Starlink-dedicated launch cadence is similar to the trend we saw last year.

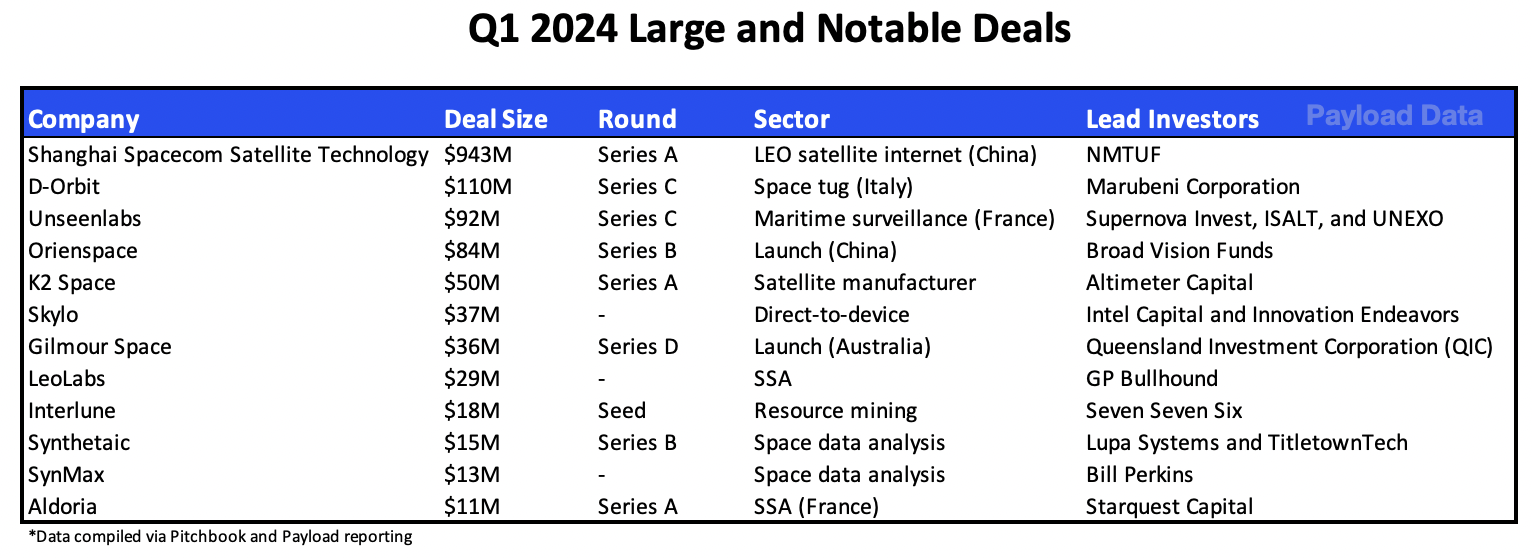

Key takeaways:

- Half the deals listed are international fundraises, including the four largest.

- Shanghai Spacecom Satellite Technology’s $943M monster raise will support its planned ~12,000 LEO G60 constellation, which is China’s response to SpaceX’s Starlink network. The group plans to launch its first 108 satellites this year.

- The list features two data analysis startups and two SSA businesses, underscoring VC interest in the data and services sectors.

- US launch and spaceflight had a quiet quarter compared to the substantial attention it has received in past years.

NASA Releases Updated Software Catalog

NASA is continuing its tradition of not gatekeeping success by unveiling a major update to its public software catalog.

Direct-to-Cell Pricing Revealed, Market Impact: Analysis

The most exciting moment of Sunday’s Super Bowl was finally getting concrete direct-to-cell pricing numbers.

Tracking US Mobile Satellite Service Spectrum

The MSS landscape is about to evolve rapidly as incumbents form new partnerships to ride the D2D wave while new entrants work to get access to the valuable MSS spectrum.

Estimating SpaceX’s 2024 Revenue

Payload is back with our SpaceX revenue breakdown. In 2024, we estimate SpaceX’s revenue reached $13.1B in 2024, up from $8.7B in 2023. Business line estimates:

The Pentagon on Tuesday released its long-awaited strategy for working more closely with the commercial space sector, which includes plans to boost cooperation during times of peace and protect commercial assets in times of conflict.

The document is the agency’s first Commercial Space Integration Strategy, DoD space policy chief John Plumb told reporters.

“Our military relies on space every single day,” Plumb said. “To protect our men and women in uniform and to ensure the space services they rely on will be available when needed, the department has a responsibility to leverage all tools available, and those tools include commercial solutions.”

Keep reading