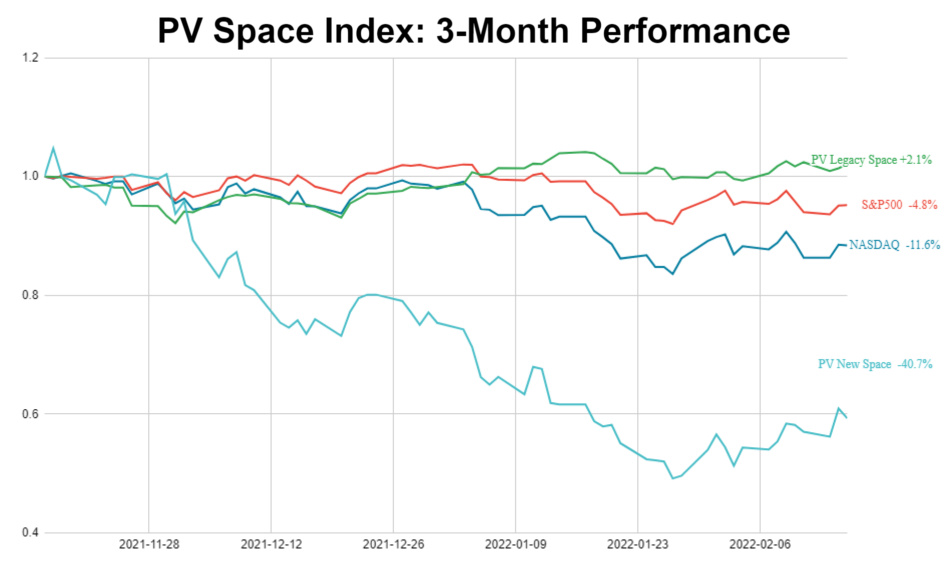

Graph: Promus Ventures. Snapshot taken Feb. 17, 2022 before market open.

As we’ve written before, investing in space is not for the faint of heart. In a recent op-ed for the FT, Sinéad O’Sullivan, a space economist, HBS senior researcher, and friend of Payload, digs a bit deeper into the dynamics of space investing.

The good: In 2021, privately held industry leader SpaceX reportedly crossed a $100B valuation after secondary share sales. Nine space companies went public via SPAC. And investors put $14.5B+ into space infrastructure companies, an annual leap of more than 50%.

- SPACs provide retail investors (and traders) an opportunity to back earlier-stage companies closer to the ground floor. Due to US securities laws, non-accredited investors have historically been barred from investing in startups.

The bad: Space, or more specifically, SPAC investing is a double-edged sword that cuts both ways. Virgin Galactic (NYSE:SPCE) traded up 32% earlier this week, but it’s also dropped by similar amounts over a single day in the past. Shares of Astra (NASDAQ:ASTR), as another example, dropped 26% last Thursday after a launch failure mid-flight.

O’Sullivan proposes a useful framework for evaluating the space investment landscape.

- Pure-play space stocks. This cohort includes the space SPACs, which make most of their money from space products/services. These are the names you’d find on Promus Ventures’ widely cited New Space Index. They have “large and concentrated exposure to unprofitable and largely unrealised sectors,” O’Sullivan writes.

- Legacy space companies, akin to “mini-ETFs.” These firms have multi-sector exposure across defense contracting, aircraft manufacturing, and the like. Space is part of a wider portfolio. That the Legacy Space Index is outperforming is not necessarily due to their space-specific business divisions, but likely due to Ukraine-Russia military tensions.

One final thought: Sure, space SPACs are down bad. It’s not unthinkable that some names in the cohort de-list, go bankrupt, or become acquisition targets. Rather than comparing the space SPACs to more established publicly traded companies, we’d also propose analyzing them alongside…

- Momentum stocks: ARK Innovation ETF (ARKK) is down 38% over the last three months.

- Sector-agnostic, small-cap, growth-stage SPACs: DSPC, an ETF that includes 25 de-SPAC’d companies, is down 42% over the same period.

- The PV New Space Index is right in the middle, at -40.7% over the last three months.

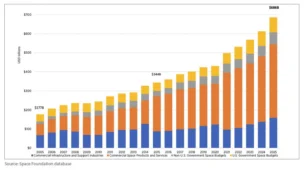

Breaking Down the $686B Space Economy

The global space economy totaled a record $686B in 2025, according to the Space Foundation.

SpaceX Alum Have Raised $9.2B, New Data Shows

As an organization that’s employed thousands of engineers in its 24-year history, SpaceX has acted as both a breeding ground for high-level engineering talent, and as a launch pad for new ideas.

Space Stocks Dip After SpaceX IPO

SpaceX’s strong first day out was coupled with a significant pullback among investors in other publicly traded space companies, sending major players down across the board.

VCs Predict the SpaceX IPO Will Lift the Entire Industry

After the public markets initiate their newest whale, what happens to the rest of the space industry still reliant on private capital?

Belgium-based geospatial analytics startup Aerospacelab announced it has raised a 40M Euro (~$45.5M) Series B co-led by Airbus Ventures and XAnge. Octave & Miroslaw Klaba, SRIW, Noshaq, BNP Paribas Private Equity, Sambrinvest, and Belaero also participated in the round.

Aerospacelab 101: Founded in 2018, Aerospacelab is already no small operation, with two offices and 110+ full time employees. The business centers on geospatial intelligence, hosting a satellite platform that incorporates artificial intelligence and machine learning to fill in the gaps.

“Awareness is only the first step,” said Benoit Deper, Aerospacelab CEO and founder, during an address at today’s ESA Space Summit. “We need to gather a lot more data to move from awareness to actionable intelligence. We need more satellites and better satellites.”

Keep reading