AST SpaceMobile announced a landmark agreement with Ligado Networks last month that will provide AST 40 MHz of L-band Mobile Satellite Service (MSS) spectrum across the US and Canada, as well as an additional 5 MHz of spectrum in the US.

Worth ~$7B ($550M upfront + $80M annually for 80 years), the deal places the value of the spectrum at roughly $2M per MHz per year.

MSS spectrum 101: Mobile Satellite Service (MSS) is the service designation for two-way comms between satellites and terrestrial platforms in motion (think handheld devices or terminals mounted on vehicles).

Historically, L-/S-band MSS spectrum was primarily used for handheld satellite phones and low-speed internet on moving platforms such as airplanes and ships. However, the high costs and subpar internet quality limited the widespread adoption of those services. In recent years, this narrative has shifted as MSS spectrum found new applications in enabling direct-to-device (D2D) satellite connectivity.

Direct-to-device: Advances in technology now allow unmodified smartphones to connect directly with satellites, delivering service in areas without terrestrial cellular coverage. The proximity of L-/S-band MSS spectrum to terrestrial cellular bands means many smartphones can enable satellite connectivity through a simple firmware update, significantly lowering barriers to adoption.

In March 2024, the Federal Communications Commission (FCC) introduced a groundbreaking rule permitting terrestrial spectrum in the 1850–2000 MHz band to be used for Supplemental Coverage from Space (SCS). This regulatory change enabled SpaceX to leverage T-Mobile’s terrestrial spectrum to provide cellular connectivity in the US from space.

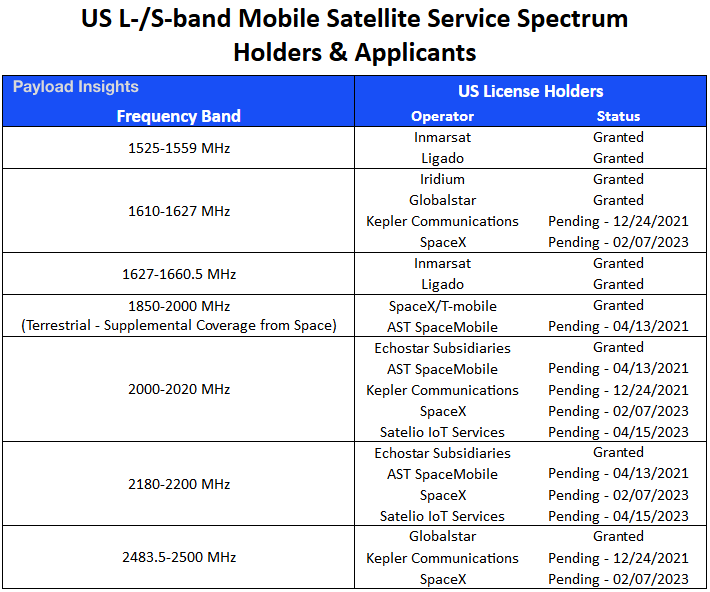

US L-/S-band MSS Allocations Overview

- 1525-1559 MHz: Globally allocated for space-to-Earth (downlink) MSS operations.

- Inmarsat and Ligado hold spectrum rights in this band.

- 1610-1660.5 MHz: Globally allocated for Earth-to-space (uplink) MSS operations, with secondary space-to-Earth (downlink) allocation in portions of the band.

- Iridium and Globalstar hold spectrum rights in the lower portion of the band, while Inmarsat and Ligado hold spectrum rights in the upper portion.

- 1850-2000 MHz: Newly allocated MSS band only in the US, on a secondary basis, to support cellular Supplement Coverage from Space (SCS). The upper end of the band (1980-2000 MHz) is globally allocated for MSS operations.

- Currently, only SpaceX through its partnership with T-mobile has been authorized to commercially use this band by the FCC.

- 2000-2020 MHz: Allocated for Earth-to-space (uplink) MSS operations in the US, with the 2000-2010 MHz portion globally allocated.

- Echostar (through its subsidiaries) holds spectrum rights for this band.

- 2180-2200 MHz: Globally allocated for space-to-Earth (downlink) MSS operations.

- Echostar (through its subsidiaries) holds spectrum rights for this band.

- 2483.5-2500 MHz: Globally allocated for space-to-Earth (downlink) MSS operations.

- Globalstar holds spectrum rights for this band.

The MSS landscape is about to evolve rapidly as incumbents form new partnerships to ride the D2D wave while new entrants work to get access to the valuable MSS spectrum.

Incumbents With Spectrum Partnership

- Globalstar/Apple: The two companies are collaborating to provide satellite-enabled features to Apple devices using Globalstar’s global satellite network. Apple is investing $1.5B to fund Globlastar’s new constellation that will be able to expand service to Apple devices.

- Echostar Consolidation: The company has strengthened its MSS portfolio and plans to build a global S-band network through acquisitions they have made over the last couple of years.

- Skylo: The Non-Terrestrial Network (NTN) service operator has partnered with MSS providers and chipset manufacturers to offer direct-to-device connectivity to a wide range of smartphones across the world. Echostar, Ligado, and Inmarsat are among the satellite partners, while Qualcomm, Samsung, MediaTek, and Sony are among the chipset partners.

- Iridium/Qualcomm (terminated): The partnership between the two companies that aimed to bring satellite-enabled features to Android phones was terminated in November 2023. Qualcomm shifted its focus to a standards-based approach for satellite connectivity versus Iridium’s proprietary solution. Starting in 2024, Iridium also shifted to an open-standards approach through Project Stardust.

New Entrants Seeking Their Own Spectrum Allocations

New entrants seeking access to MSS spectrum face strong opposition from incumbents such as Globalstar, Iridium, and Echostar, which are focused on protecting their spectrum rights.

- SpaceX: While the FCC dismissed its application for MSS spectrum, the company has launched its D2D service through a partnership with T-Mobile in the US. SpaceX has similar partnerships with cellular carriers across the world, such as Rogers in Canada and One NZ in New Zealand.

- AST SpaceMobile: The company has applied for MSS spectrum to enable D2D communications but has not received FCC approval. In the interim, it is moving forward with its plans through the partnership with AT&T and Verizon. The company recently received a special temporary authorization from the FCC to begin testing D2D service using the first five BlueBird satellites launched in September. Pending regulatory approval, AST’s long-term MSS spectrum lease agreement with Ligado will support the expansion of its service both domestically and internationally.

- Kepler Communications: Kepler filed an MSS application in 2021 but recently pivoted to focus on optical relay communication services. However, the original MSS application remains under FCC review, and the company may continue pursuing its MSS plans, given the high value of the spectrum and its early application date.

- Sateliot IoT Service: The Spanish startup applied in 2023 for MSS spectrum in the US to provide IoT narrowband satellite services, joining the growing list of companies seeking MSS spectrum access.

SpaceX D2D: A Two-Way Approach

SpaceX was the first company to receive regulatory approval for direct-to-device services using terrestrial spectrum through its partnership with T-Mobile. This collaboration enables users in the US to send messages via Starlink D2D services in areas lacking terrestrial cellular coverage.

While this partnership jump-starts SpaceX’s D2D ambitions, the company’s long-term vision is to operate using its own non-terrestrial Mobile Satellite Service (MSS) spectrum. However, on March 26, 2024, the FCC dismissed SpaceX’s application for MSS spectrum, citing the need for a new rulemaking process to assess whether a new system could coexist with incumbent networks.

In response, SpaceX filed a petition for rulemaking, urging the Commission to revise its licensing and spectrum-sharing framework for “Big LEO” non-geostationary satellite orbit (NGSO) MSS systems operating in the 1610–1617.775 MHz and 2483.5–2500 MHz bands.

There are several advantages to securing non-terrestrial MSS spectrum over use of costly terrestrial spectrum:

- Cost efficiency: Terrestrial spectrum is auctioned at high prices, often costing billions of dollars for just a few MHz. In contrast, non-terrestrial MSS spectrum involves relatively modest regulatory fees compared to terrestrial spectrum, making it a more cost-effective solution.

- No-blackout zones: Terrestrial spectrum is regulated country by country, requiring satellites to maintain blackout zones near borders to avoid interfering with neighboring terrestrial networks.

- Global harmonization: Non-terrestrial MSS spectrum is largely harmonized worldwide, enabling more seamless global expansion.

Final thoughts: The rise of direct-to-device applications has breathed new life into MSS spectrum, making it a valuable asset for incumbents and highly sought after by new entrants. Regulations must balance protecting existing systems with enabling new ones to deliver much-needed supplemental coverage from space. SpaceX has once again paved the way, and in the coming years, many more operators will introduce D2D satellite-enabled services to the market.

Exclusive: Austria Taps R-Space for Its Second Military Sat

Aurora is one of three missions in a series of planned government-backed demos to validate new technologies in orbit

Rocket Lab Enters the Satcom Market With $8B Iridium Deal

Rocket Lab ($RKLB) has been teasing its entrance into the “space applications” market for years. Yesterday, it pulled the trigger.

SpaceX Alum Have Raised $9.2B, New Data Shows

As an organization that’s employed thousands of engineers in its 24-year history, SpaceX has acted as both a breeding ground for high-level engineering talent, and as a launch pad for new ideas.

Japan Eyes Sovereign D2D Satellite Network

Japan plans to select a proposal this month for its domestically owned and operated D2D satellite network, called J-LEO.

The government should award contracts to a variety of launch vendors to support competition in an industry that is dominated by SpaceX, according to a report released Tuesday by Georgetown University’s Center for Security and Emerging Technology.

Pros and cons: The US is the leader of today’s international launch market, racking up superlatives from the highest number of annual launches to the largest mass to orbit to the most satellites in orbit.

But in this case, America’s success is SpaceX’s success. More than five out of every six US launches is a SpaceX mission, according to the report.

Keep reading