Last week, SES announced an investment and strategic partnership with direct-to-device startup Lynk Global. The relationship will allow Lynk to leverage SES’s MEO relays for routing traffic from its LEO satellites, integrate with SES’s ground systems, and expand its manufacturing footprint into Europe.

SES sees Lynk as an avenue to enter the direct-to-device gold rush. Lynk sees Europe as a way to gain access to a large market while mitigating some of the upfront capital costs.

Déjà vu: The move follows a string of US space businesses announcing their expansion into the EU in the past few weeks:

- On Mar. 3, AST SpaceMobile announced a joint venture with Vodafone and plans to open a satellite manufacturing facility in Barcelona.

- On Mar. 11, Rocket Lab announced plans to buy German-based laser comms terminal provider Mynaric in its first foray into Europe.

Europe on the rise: After years of investor malaise and memes about the region’s lack of innovation, investing in the EU is suddenly back in vogue.

- The STOXX Europe 600, a broad EU index, is up 8.5% on the year. Meanwhile, the S&P 500 is down 4.3%.

- EU defense stocks have surged this year, with names like Thales and Rheinmetall up 95.4% and 154.2%, respectively.

- European satcom providers have also jumped this year. SES and Eutelsat’s share prices have risen 89% and 150%, respectively. Eutelsat said it was actively collaborating with the EU to deploy additional terminals for critical missions such as Ukraine comms as Europe attempts to wean off its Starlink reliance.

The common thread? The surge in European optimism in the past few months stems from an asset allocation shift away from risk-on US businesses, the prospects of a significant bump in defense spending, and a belief that the region will invest in sovereign capabilities as EU countries no longer feel like they can fully rely on the US for support.

Europe’s push for independent space capabilities creates new opportunities for US-based space businesses. In addition to access to large government deals and a burgeoning commercial market, Europe offers a highly skilled workforce at significantly lower labor costs than the US, making it an attractive destination for expansion.

Years in the making: The shift to EU space enthusiasm isn’t entirely new. Investment in space startups has surged in recent years as the bloc shifts toward a more commercially driven model.

- After OneWeb filed for bankruptcy in 2020, the UK government bought the company, aiming to strengthen its commercial space sector following Brexit and the loss of joint EU projects. In 2023, OneWeb merged with French GEO operator Eutelsat.

- Last year, the European Union awarded a concession contract for its sovereign satellite communications system, IRIS², which is comprised of 290 satellites across multiple orbits. In a first for the EU, the €10.6B ($11.6B) project will be developed in collaboration with the SpaceRISE commercial consortium (SES, Eutelsat, and Hispasat), which will finance nearly half of the program. The consortium will also use the IRIS² satellites to generate commercial revenue.

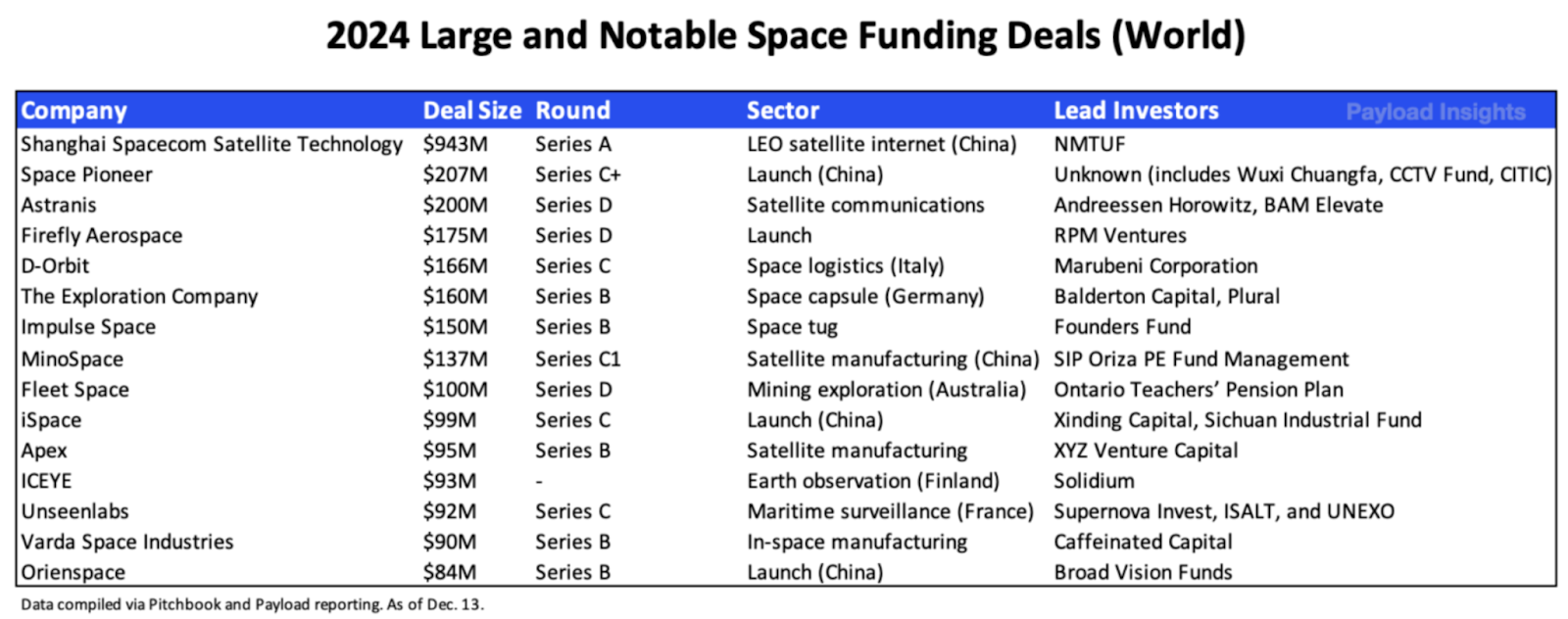

The shift in commercial sentiment and the region’s relatively underdeveloped space infrastructure have spurred a wave of investment in space startups. Last year, the Europe accounted for four of the 15 largest global space funding deals, matching the US count.

“The European space industry has been finding its ground back over the last couple of years,” Filip Kocian, a European investor at Expansion Ventures, told Payload in an emailed statement. “Two initiatives which I think aren’t widely appreciated are the Cassini programme which invested hundreds of millions of EUR to co-anchor space and space-adjacent VCs funds in the EU. [And] after COVID-19, many nations decided to spend their recovery funding on boosting the domestic space industries.”

However, not all news has been positive for the European space sector. Airbus’s space program faced significant challenges in 2024. In the fourth quarter alone, the company absorbed $300M in space charges. We’ve seen a similar trend with US aerospace primes, like Boeing, taking substantial financial hits on their space programs.

The sovereignty argument: Last month, the European Commission introduced ReArm Europe, an €800B ($876B) investment to strengthen Europe’s sovereign defense capabilities. While talks of increasing defense spending have been around for years, shifts in US foreign policy may accelerate its implementation, opening new opportunities for European and potentially US space companies.

While deals like the OneWeb-Eutelsat merger, the IRIS² satellite system, and the influx of US space firms expanding into Europe support the region’s sovereignty goals, one critical piece remains missing—a reliable European launcher.

Over the past few years, the EU faced a sovereign gap as Arianespace transitioned from Ariane 5 to Ariane 6, forcing Europe to rely on SpaceX for access to orbit. In response, European launch startups are racing to bring new launch capabilities online, with ISAR Space set to launch its first rocket from Andøya, Norway, in the coming days.

It goes both ways: There’s a growing revolving door between the European and US space industries. For years, European space companies have expanded into the US to secure lucrative DoD contracts and attract investment, with D-Orbit, AerospaceLab, and EnduroSat among the more recent examples. However, the latest moves by Lynk, AST SpaceMobile, and Rocket Lab highlight an emerging reverse trend—US space companies are now looking to Europe, drawn by potential government contracts and the opportunity to establish themselves as market leaders.

NASA Puts $2B Price Tag on Nuclear Mars Mission

The $2B Space Reactor-1 Freedom is said to be the first fission-powered interplanetary spacecraft.

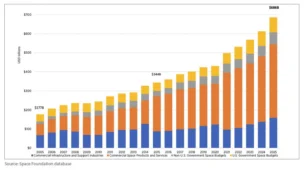

Breaking Down the $686B Space Economy

The global space economy totaled a record $686B in 2025, according to the Space Foundation.

UK Commits £62M into Domestic Space Capabilities

The UK government announced £62M ($83.3M) in new funds Monday to develop domestic satcom and space technologies.

NASA Selects Starlink for Artemis III Mission

NASA has awarded SpaceX a contract to deliver laser communications capabilities for its Artemis III mission using Starlink.

The Canadian space program is growing at a hypersonic pace.

NordSpace, the Ontario-based space tech startup, is establishing the Supersonic and Hypersonic Applications Research Platform (SHARP), which aims to grow the country’s hypersonic capabilities with three new products.

“There’s been a lot more interest in national sovereignty and understanding what our own capabilities are here, so that we’re more resilient at home, but also, in NordSpace’s opinion, more capable allies to partners like the United States,” Rahul Goel, NordSpace’s CEO, told Payload.

Keep reading