The most exciting moment of Sunday’s Super Bowl was finally getting concrete direct-to-cell pricing numbers.

T-Mobile announced the following pricing plans for Starlink’s no-dead zone connectivity.

- Free on T-Mobile’s highest level premium Go5G Next plan

- $10-$15/mo per line for all other T-Mobile plans

- $20/mo per line for all other carriers like AT&T and Verizon. (Power move to open the service up to non-T-Mobile plans via eSIM tech in this hotly contested market).

T-Mobile’s stock jumped 3% on the news for an $8B increase in market value. Not bad value for a Super Bowl ad: spend $8M, get $8B.

The pricing also provided long-awaited insights on what to expect from other direct-to-cell players like AST SpaceMobile, Globalstar, Iridium, Skylo, Viasat, Echostar, and Kuiper. We covered the industry’s direct-to-device spectrum scramble last week, which goes into detail on the regulatory and competitive landscape.

Upsell With Space

The pricing scheme is set up to encourage more customers to switch to or sign up for T-Mobile’s highest premium plan. $10-$15 is a high monthly charge to ask customers to pay, but it has the effect of making the ultra-premium plan look more attractive.

Roughly 60% of new T-Mobile customers and nearly 80% of Verizon customers are on premium plans. Pushing customers to higher premium offerings is an important growth driver for carriers

Marketing benefit: The Starlink 🤝 T-Mobile go-to-market strategy will also be a strong lead generator for the company. The company directed 128M Super Bowl watchers to sign up for a few months of free Starlink service, regardless of carrier. So, as a curious and susceptible consumer, I did. T-Mobile had me fill out a sign-up form with my number, including a footnote disclosing that they may reach out with T-Mobile offers. I’m a Verizon customer, but now a prime target.

Who’s paying the add-on? While increasing the value of the premium plan is low-hanging fruit, we will have to wait and see how many people are willing to cough up ~$15 per month for the no-dead zone service.

When it comes to an active decision to spend money on an opt-in service, most consumers don’t care that connectivity is beamed down from space; the primary consideration is whether the service solves a genuine frustration in the consumer’s life. That goes for both wealthy and middle-class consumers.

How big is the problem?

- In the US, phone users experience call dead zones ~1% of the time, according to OpenSignal and PC Mag studies. Data dead zones are higher.

- It’s both a rural problem (lack of cell towers) and an urban problem (congestion). But for the majority of cell phone users, dead zones are not a big irritation.

But if you live in a notorious dead zone, the $15 monthly add-on may be worth it. The market is big enough that only a small percentage of sign-ups can generate significant revenue, although it has not yet been revealed what percent of service revenue DTC providers take home.

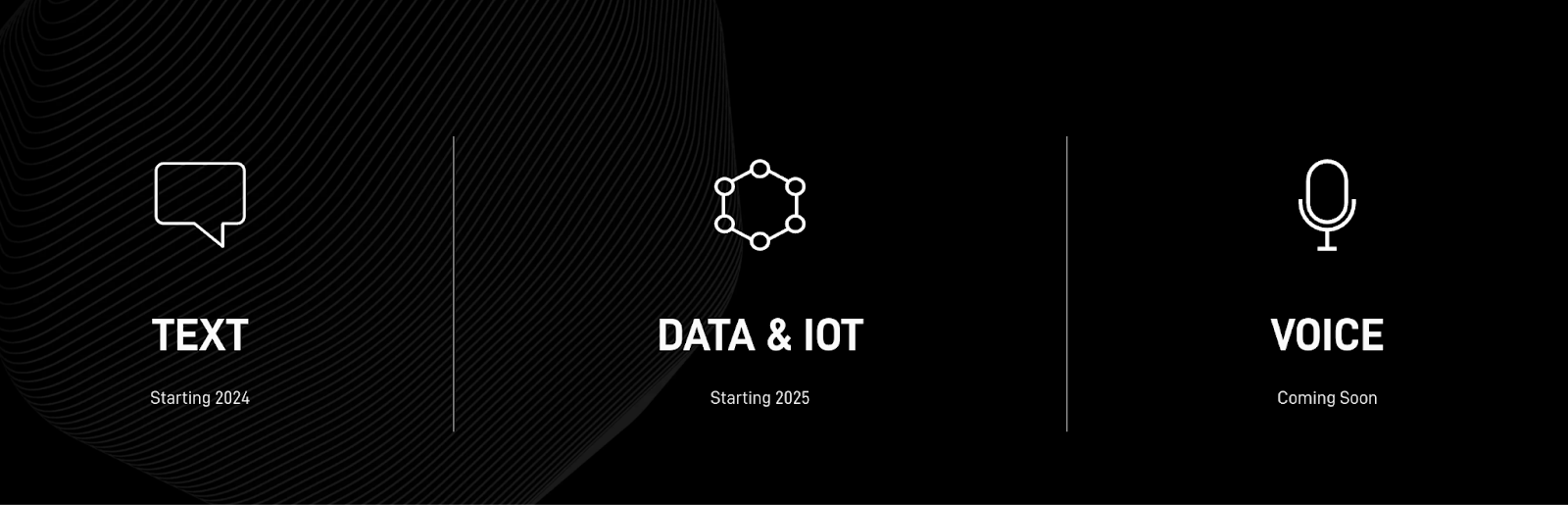

The Starlink service will begin as text-only. Data connectivity is slated to roll out later this year and calling in 2026+. To support the service to date, SpaceX has launched over 450 direct-to-cell satellites.

Market Size

The telco industry is a hotly competitive, often petty market. It is usually hard to find ways to differentiate. Offering no dead zones service in a premium plan is enough to set a provider apart. As a result, Verizon and AT&T will inevitably need to provide the same service. For direct-to-cell satellite operators, the untapped market is enormous.

Mobile network operator subscribers:

- Verizon: 146M

- T-Mobile: 130M

- AT&T: 118M

The market grows much bigger when you look abroad. DTC providers see the opportunity for billion-dollar businesses to be built by siphoning off a tiny fraction of the $1T global wireless service market.

AST SpaceMobile: Direct-to-cell startup AST SpaceMobile’s ($ASTS) stock is up 700%+ over the past 12 months, due to increasing optimism about market size and its tech. The company, which has secured partnerships with Verizon and AT&T, has an $8.7B market cap, making it the third most valuable space business after SpaceX and Rocket Lab.

AST stock jumped over 20% on rosier-than-expected ARPU assumptions after the Starlink ~$15/mo per line structure was announced.

Given the sheer size of the market, even a small ARPU can generate big returns.

- For example, $1 ARPU per month could generate $1B+ per year if AST can connect 100M customers via premium plans.

AST is building satellites with enormous antennas specifically designed for providing 4G/5G DTC connectivity. The company has just five operational DTC satellites in orbit, needing 20 for half coverage and 40+ for full coverage. It will take a few years to deploy the constellation.

AST economics:

- The company has signed contracts to launch 45 to 60 BlueBird satellites through 2026.

- The average direct materials and launch cost per satellite is $19M-$21M. 60 satellites x $20M = $1.2B.

- AST says it can break even with 20 satellites providing half coverage.

Other competitors: You also have other competitors like Globalstar, Iridium, Skylo, Viasat, Echostar, and Kuiper that are building DTC capabilities. While Starlink has a stronghold on broadband capability, competitors see an angle with the potentially huge market size of backup mobile connectivity.

Final thoughts: More than anything, the T-Mobile commercial served as a loud introduction of direct-to-cell service to the public—a starter pistol for the market. Beyond offering the service free of charge to boost its highest premium tier, the real test to gauge market size will be opt-in demand.

Contrivian Launches New Product Bundling Amazon Leo & Starlink

Customers looking for satellite connectivity are often forced to choose between one provider or another. Those days are over.

Viasat and Space42 Share Strategy for Equatys JV

The two companies cancelled a key roundtable at the Mobile World Conference, but Viasat CEO Mark Dankberg gave Payload an exclusive rundown.

Mynaric Demos QKD Comms With COTS Tech

German engineering just entered the quantum realm.

OQ Technology Lands €25M in EIB Venture Debt Financing

Europe is driving hard on direct-to-device (D2D).

China’s space program had a busy start to the year, and it isn’t letting off the gas anytime soon.

The nation has already launched six times in 2025. Just this week, the Long March 8A rocket made its maiden flight. The upgraded version of the Long March 8 includes a more powerful second stage and a larger payload fairing, allowing the rocket to bring 7,000 kg to SSO.

More to come: The Long March 8A flight is expected to be the first of many debut flights for Chinese launchers this year. While China’s Long March series of rockets has accounted for most of the launches from the country in recent years, the explosive growth of its commercial capabilities is expected to give the nation more options for low-cost launches going forward.

Keep reading