Last week, Payload cofounder Mo Islam had the pleasure of sitting down with three top VCs: Anton Brevde from Prime Movers Lab, Michelle Volz from a16z, and Shahin Farschi from Lux Capital. The hour-long conversation covered the state of the economy, the fundraising environment for space companies, and predictions for 2023.

We’ve curated some of the key highlights from that discussion below.

Fundraising

- It will be difficult to raise this year. Expect a general flight to quality and a spike in down rounds in the second half of 2023.

- Only 11% of late-stage funding rounds last year were down rounds (startups that raised generally avoided priced rounds via bridge financing led by insiders). Founders who proactively raised will be in a much more advantageous position…even if they had to raise a structured or flat round.

- Many companies were so well-funded at the tail-end of the fundraising boom period that they did not need to raise capital last year. A tremendous number of companies have six or fewer months of runway remaining this year and will need to raise. Those companies will be forced to take unfavorable terms to get deals across the finish line.

- Investors will pay closer attention to product timelines, especially as it relates to capital-intensive businesses. Later-stage investors will be much more disciplined and early-stage investors have to be mindful of where the capital will come from down the road.

Public Markets

- Before the SPAC boom, space companies faced a dearth of liquidity. SPACs allowed investors and management teams to chase short-term liquidity in exchange for capital discipline.

- Now, the downstream effects of that are retail investors losing money, along with crossover and growth funds. It may take time for the institutional capital to come back to the table.

- Expect to see consolidation and some bankruptcies this year. Public companies are running out of cash, and the capital markets will not be open to them. Meanwhile, activity in aerospace and defense (A&D) private equity has doubled in the past 5 years. Read more about that topic here.

Trends & Predictions

- Space is maturing as a category of investment. Take mobile as an example. It was once a broader category of investment, but now there’s all kinds of verticals in mobile that are defined by the markets they’re selling into. A satellite company today may be a media company or an enterprise company tomorrow.

- Long-term liquidity for space investors should ultimately not be too much of a concern. Even though SpaceX has been private for 20 years, investors have had many opportunities to generate liquidity through secondary sales. Today’s best companies will have robust secondary markets tomorrow.

- Opportunities worth exploring include sovereign launch capabilities in Europe, India, and the Middle East; “endless propulsion” in VLEO; directed energy; space domain awareness (SDA); and traffic management (STM)

- Starship will create a race to the bottom and immense downward pressure on pricing for launch providers. The vehicle itself and its advertised capabilities may also open up radical new business models. But without an operational Starship, SpaceX could face significant financing risk (read Anton Brevde’s take on this here).

Ultimately, though guests diverged on certain theses and areas of focus, what was clear from all three is that 2023 will be a difficult year for space companies looking for financing. Many startups will be forced to raise with unfavorable terms and some won’t be able to tap the capital markets at all. One of the biggest risks for industry growth in the near-term is that capital becomes too expensive and that’s certainly where the eight ball appears to be heading.

Stay tuned for more from us, as these topics will be an ongoing theme not only in Payload, but among future webinar guests. And if you’d like to watch the full webinar, you can do so by clicking the link below.

Sophia Space Raises $7M, Taps Apex for 2027 Demo Flight

The orbital-compute startup today announced new fundraising—as well as a demo flight with Apex. Both initiatives are aiming to position the company to begin deploying its edge compute hardware in-orbit.

Ubotica Raises $11M for Satellite-Based AI Tech

The Dublin-based space AI company raised $11M today to accelerate the commercialization of its AI-powered intelligence platform for maritime security.

ElevationSpace Closes $40M Series B

The Japanese satellite reentry startup raised a $40M Series B, bringing the company’s total amount raised to $63.5M.

Instinct Space Unveils Plans for Low-Cost Lunar Landers

Instinct Space announced a significant pivot today from helping lunar surface missions find their way to getting in on the surface action itself.

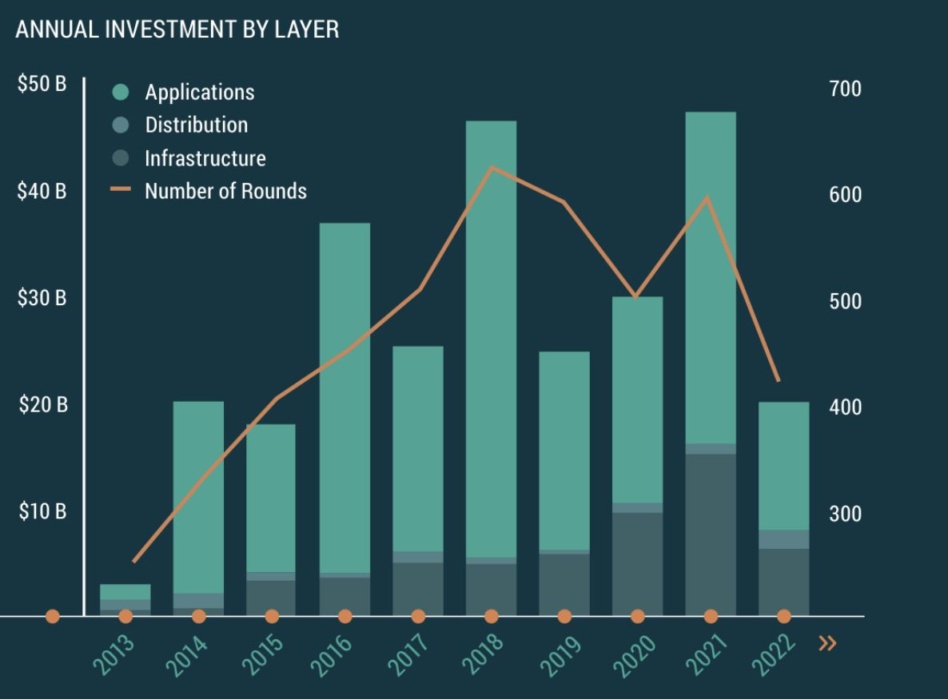

Space Capital has released its final quarterly report on the 2022 investing landscape. It was a tough year for fundraising, as the froth drained from the free-flowing capital markets of years past. Though the space industry saw receding levels of capital deployment, the report’s authors remain optimistic about the sector’s ability to bounce back.

As capital markets tightened up last year, the space sector saw a dramatic drop in VC deals and funding…especially when sized up against the soaring highs of 2021. All in all, the space sector raised $20.1B across 420 rounds last year.

Later stage companies were impacted most by the drawdown, and early-stage companies pulled in only 4% less in capital than the year before. Seed and Series A rounds accounted for more than half of total rounds, at 41% and 25%, respectively.

Keep reading